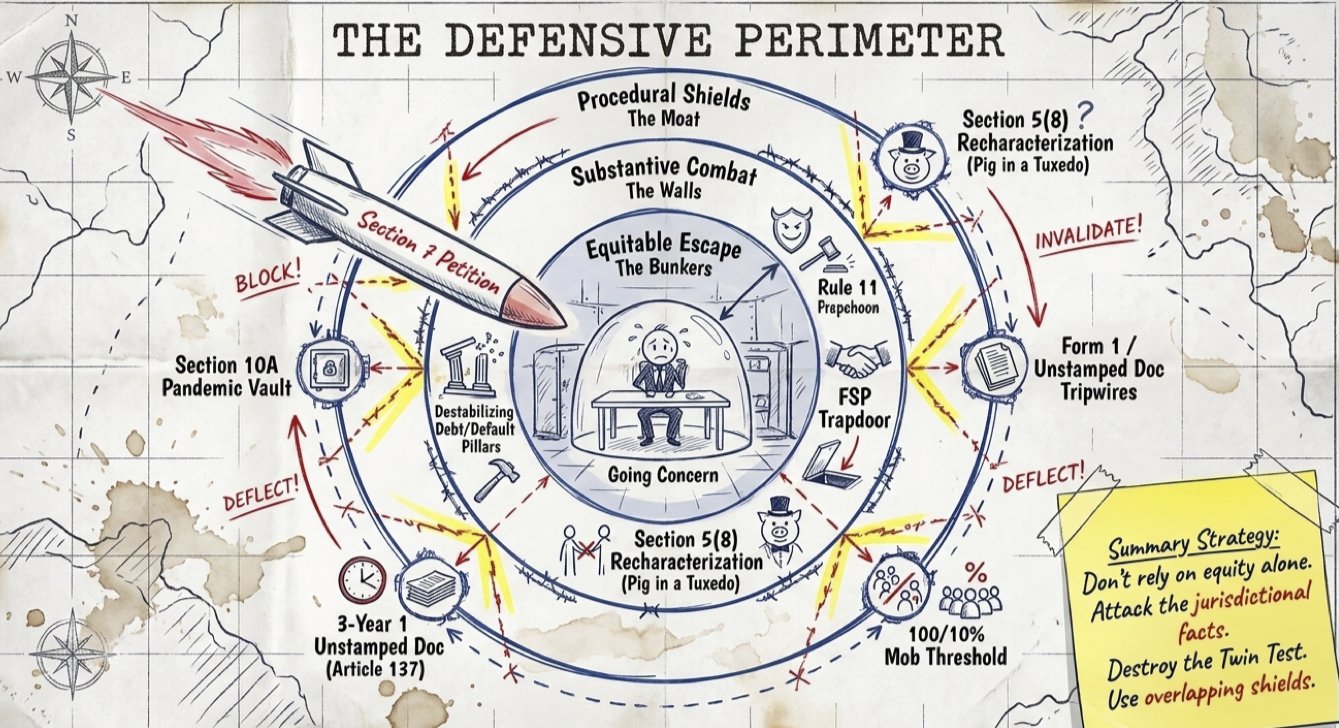

- Section 7 under the IBC empowers financial creditors to initiate CIRP, suspending the board and vesting control in an IRP.

- Admission hinges on the Twin Test: existence of a financial debt and occurrence of default, per Innoventive.

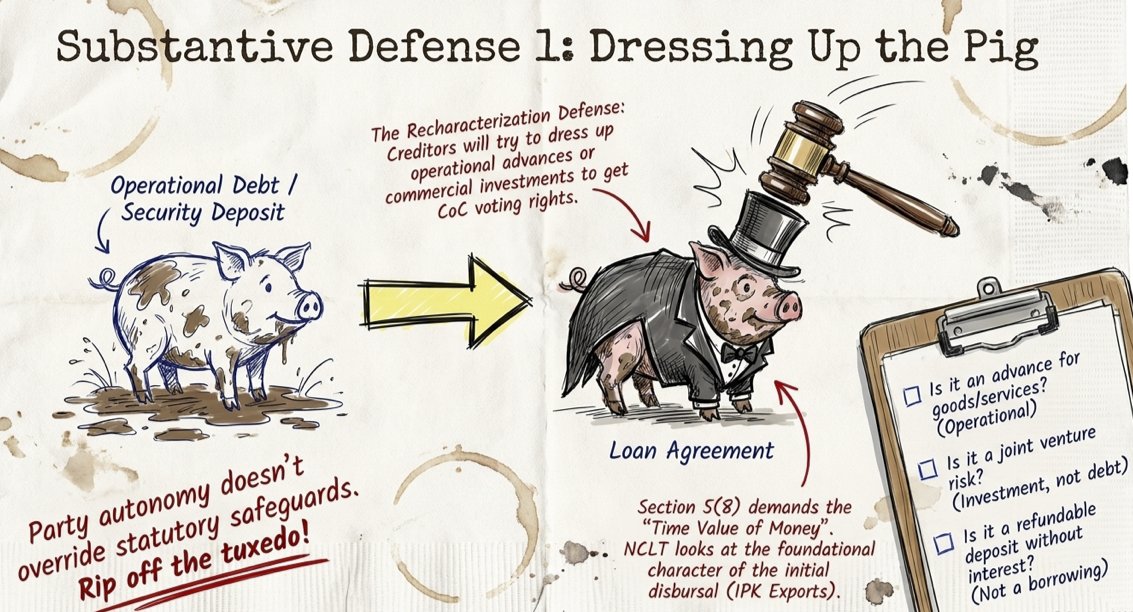

- Challenge classification: recharacterize operational advances, investments, or deposits to defeat a financial debt under Section 5(8).

- Third-party mortgages lack standing to trigger CIRP; Anuj Jain confirms mortgagees are secured creditors, not financial creditors.

- Limitation defense: the Limitation Act applies via Section 238A; Article 137 imposes a three-year bar from the date of default.

- Section 10A grants perpetual immunity for defaults between March 25, 2020 and March 24, 2021; such defaults cannot ground petitions.

- Invoke Section 65 against fraudulent or malicious petitions; penalties deter misuse and protect debtors from harassment.

DEFENDING SECTION 7 IBC PETITIONS: A GUIDE FOR CORPORATE DEBTORS

Creditor and contributor of this article:

Patra’s Law Chambers:

About Us:

Patra’s Law Chambers is a law firm with offices in Kolkata & Delhi, offering comprehensive legal services across various domains. Established in 2020 by Advocate Sudip Patra (Advocate, Supreme Court of India & Calcutta High Court) an alumnus of the Prestigious Rajiv Gandhi School of Intellectual Property Law, IIT Kharagpur ,with Post Graduate diploma in Business Law from IIM Calcutta, the firm specializes in Civil, Criminal, Writs,High Court Matters, Trademark, Copyright, Company, Tax, Banking, Property disputes, Service law, Family law, and Supreme Court matters.You can know more about us in here

Kolkata Office:

NICCO HOUSE, 6th Floor, 2, Hare Street, Kolkata-700001 (Near Calcutta High Court)

Delhi Office:

House no: 4455/5, First Floor, Ward No. XV, Gali Shahid

Bhagat Singh, Main Bazar Road, Paharganj, New Delhi-110055

Website: www.patraslawchambers.com

Email: [email protected]

Phone: +91 890 222 4444/ +91 7003 715 325

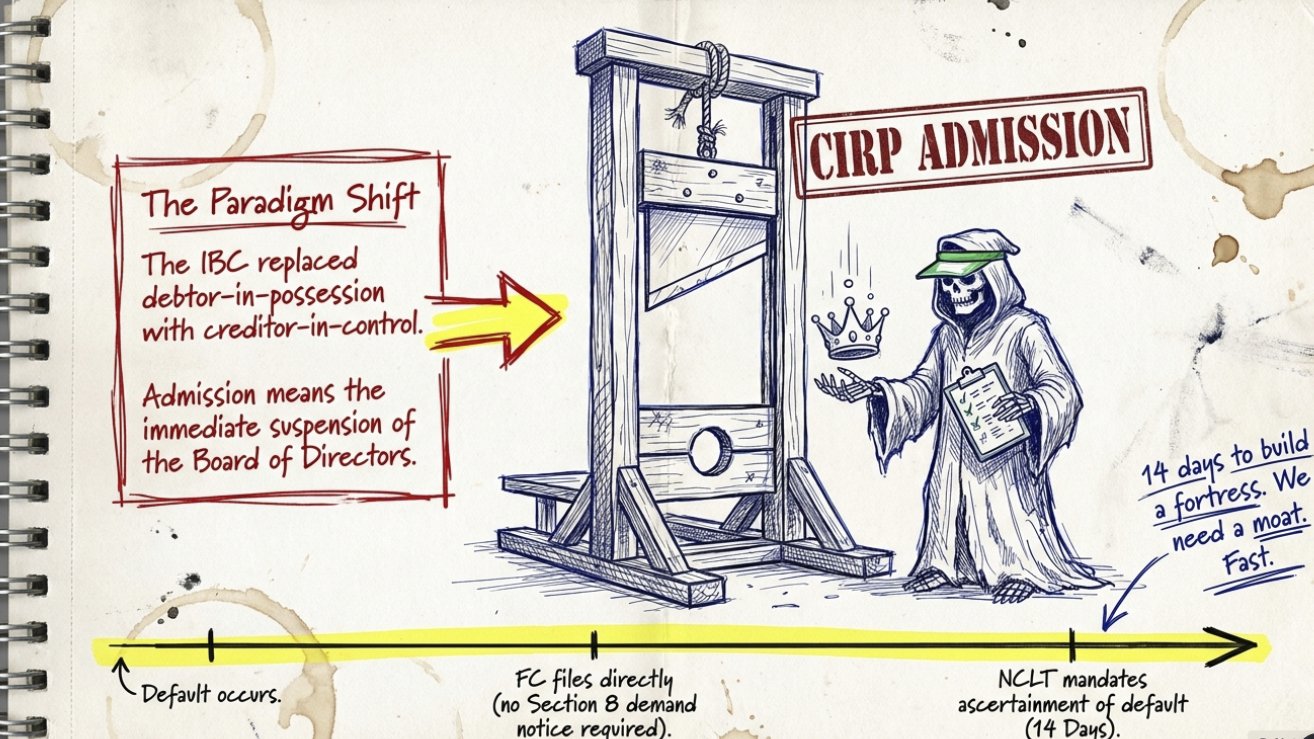

The enactment of the Insolvency and Bankruptcy Code, 2016 (IBC), inaugurated a transformative era in the Indian credit landscape, effectively replacing the erstwhile debtor-in-possession regime with a creditor-in-control model. At the heart of this legislative architecture is Section 7, which empowers financial creditors to trigger the Corporate Insolvency Resolution Process (CIRP) upon the establishment of a default. For a corporate debtor, the admission of a Section 7 petition is a watershed moment that results in the immediate suspension of the board of directors and the transfer of management control to an Interim Resolution Professional (IRP).1 Consequently, the defense against such a petition is not merely a legal dispute over a financial obligation; it is a fundamental struggle for corporate survival and the preservation of the entity as a going concern.

The Foundational Shift and Statutory Framework of Section 7

Section 7 is a unique mechanism designed to facilitate the rapid identification of financial stress and the time-bound resolution of insolvency. Unlike operational creditors, who must issue a demand notice under Section 8 prior to filing a petition under Section 9, financial creditors can approach the National Company Law Tribunal (NCLT) directly once a default occurs.1 This streamlined access is predicated on the belief that financial creditors, typically banks and financial institutions, possess the sophisticated monitoring capabilities required to identify insolvency at an early stage. The definition of a “financial creditor” under Section 5(7) is inextricably linked to the concept of “financial debt” defined in Section 5(8), which fundamentally requires the disbursal of funds against the consideration for the “time value of money”.3

The adjudication process under Section 7 is characterized by its summary nature. The Adjudicating Authority is mandated under Section 7(4) to ascertain the existence of a default within fourteen days of the receipt of an application, primarily by relying on the records of an information utility or other evidence provided by the creditor.1 This truncated timeline places an immense burden on the corporate debtor to present a robust defense quickly and effectively. While the legislative intent emphasizes speed, the judiciary has consistently maintained that the NCLT is not a mere rubber stamp and must satisfy itself regarding the jurisdictional facts of debt and default.8

| Statutory Provision | Function in Section 7 Proceedings | Implications for the Debtor |

| Section 5(7) | Defines “Financial Creditor” based on the nature of the debt. | Allows challenging the locus standi of the petitioner. |

| Section 5(8) | Defines “Financial Debt” as disbursal for time value of money. | Core ground for recharacterizing the debt as operational or investment. |

| Section 7(4) | Mandates NCLT to ascertain default within 14 days. | Imposes strict timelines for preparing and filing a response. |

| Section 7(5) | Provides the AA with the power to admit or reject the petition. | Central point of debate regarding judicial discretion (Vidarbha doctrine). |

The Threshold of Admission: Navigating the Twin Test

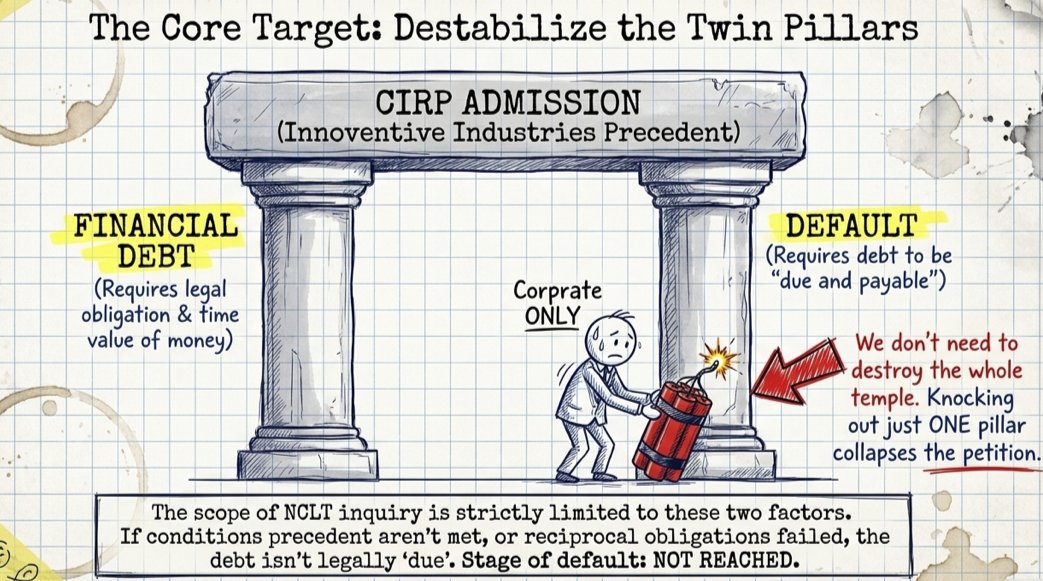

The admission of a Section 7 petition hinges on what is commonly referred to as the “Twin Test”: the existence of a financial debt and the occurrence of a default. In the seminal case of Innoventive Industries Ltd. v. ICICI Bank, the Supreme Court clarified that the scope of inquiry under Section 7 is limited to these two factors. Once the NCLT is satisfied that a default has occurred and the application is complete, it is generally obligated to admit the petition.8 This narrow focus differentiates Section 7 from civil suits, where complex questions of fact and equity might be entertained. For the corporate debtor, the strategy must therefore focus on destabilizing one of these two pillars.

The existence of a “debt” is not merely a question of whether money was transferred. It requires a legal obligation in respect of a claim which is due from any person.7 A “default” occurs when the whole or any part or installment of the amount of debt has become due and payable and is not paid by the debtor.8 The defense must scrutinize the “due and payable” aspect. If a debt is subject to conditions precedent that have not been fulfilled, or if the creditor has failed to perform reciprocal obligations under a contract, the debt may not be legally “due” in the eyes of the law. This creates a strategic opening for the debtor to argue that while a financial transaction took place, the stage of default has not yet been reached.8

Substantive Defenses: Re-evaluating “Financial Debt”

A primary and often successful defense for a corporate debtor is to demonstrate that the underlying transaction does not qualify as a “financial debt” under Section 5(8). If the transaction lacks the essential characteristics of a financial debt, the creditor cannot maintain a petition under Section 7.1

The Requirement of Time Value of Money

The core of a financial debt is the disbursal of funds against consideration for the “time value of money”.5 This implies that the money was provided for a specific period with the expectation of a return, usually in the form of interest. However, the absence of interest does not automatically disqualify a debt from being “financial” if the transaction otherwise has the “commercial effect of a borrowing”.5

Corporate debtors can challenge the classification of a debt by showing it originated from a different commercial context:

- Operational Advances: If the amount claimed was an advance paid for the supply of goods or services, it constitutes an operational debt. Even if the parties later enter into a loan agreement to “convert” this debt, the NCLT often looks at the foundational character of the transaction at the time of initial disbursal. In IPK Exports Pvt. Ltd. v. HSB Home Solutions Ltd., the tribunal refused to allow the conversion of an operational advance into a financial debt without a fresh disbursal of funds.13

- Commercial Investments and Joint Ventures: Funds infused as equity or as a share in a joint venture are not financial debts because the “lender” is essentially a partner in the business risk. In Bhuvan Kumar Gupta v. Maverick Developers, the court scrutinized the nature of the investment to determine if the parties intended a debtor-creditor relationship or a joint-development partnership.5

- Refundable Security Deposits: A security deposit that is not linked to any interest-bearing facility or a loan agreement may not have the commercial effect of a borrowing. In Global Credit Capital Ltd. v. Sach Marketing Pvt. Ltd., the Supreme Court emphasized that for a claim to be a financial debt, the disbursal must be for the time value consideration and not merely a deposit for services.14

The Recharacterization Defense and Party Autonomy

A significant tension exists between the principle of party autonomy—the freedom of parties to contract and label their transactions—and the regulatory safeguards of the IBC. While parties may label an agreement as a “loan,” the Adjudicating Authority is empowered to look beyond the form and examine the substance of the transaction.13 This is particularly relevant when creditors try to “dress up” operational debts to gain the voting rights and priority in liquidation associated with financial creditors. The defense must argue that permitting such recharacterization would erode the statutory scheme and turn the IBC into a blunt tool for debt recovery rather than an insolvency resolution framework.13

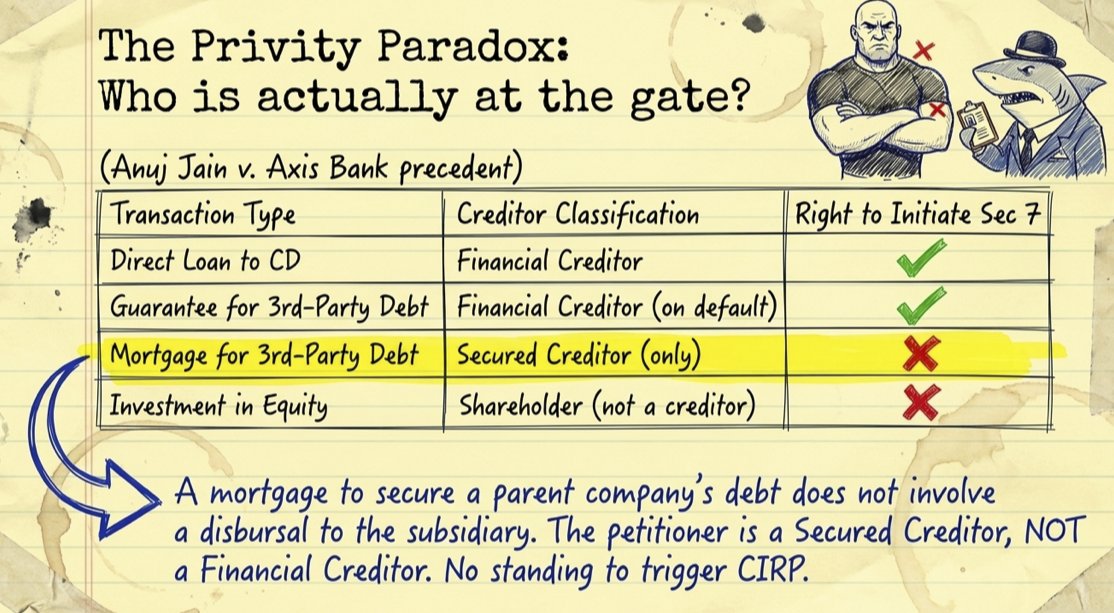

The Privity Paradox: Third-Party Mortgages and Security Interests

One of the most potent legal ideas in the defense of corporate debtors involves the distinction between a “secured creditor” and a “financial creditor.” This was authoritatively resolved by the Supreme Court in Anuj Jain v. Axis Bank Ltd., a judgment arising from the insolvency of Jaypee Infratech Limited (JIL).15

In this case, JIL had mortgaged its land as collateral security to lenders of its holding company, Jaiprakash Associates Limited (JAL). The lenders argued that they were financial creditors of JIL by virtue of these mortgages. The Supreme Court rejected this, holding that for a person to be a “financial creditor,” the corporate debtor must owe them a “financial debt.” A mortgage created to secure the debt of a third party does not involve a disbursal of funds to the mortgagor against the consideration for the time value of money.15

| Transaction Type | Creditor Classification under IBC | Right to Initiate Section 7 |

| Direct Loan to Corporate Debtor | Financial Creditor | Yes |

| Guarantee for Third-Party Debt | Financial Creditor (upon default) | Yes |

| Mortgage for Third-Party Debt | Secured Creditor (only) | No |

| Investment in Equity | Shareholder (not a creditor) | No |

This distinction is crucial for corporate debtors. If a petitioner is a mortgagee who did not lend money directly to the debtor, they lack the standing to trigger CIRP. This defense effectively protects subsidiaries from being dragged into insolvency solely due to security interests created for the benefit of their parent companies, provided no direct financial debt or guarantee exists.15

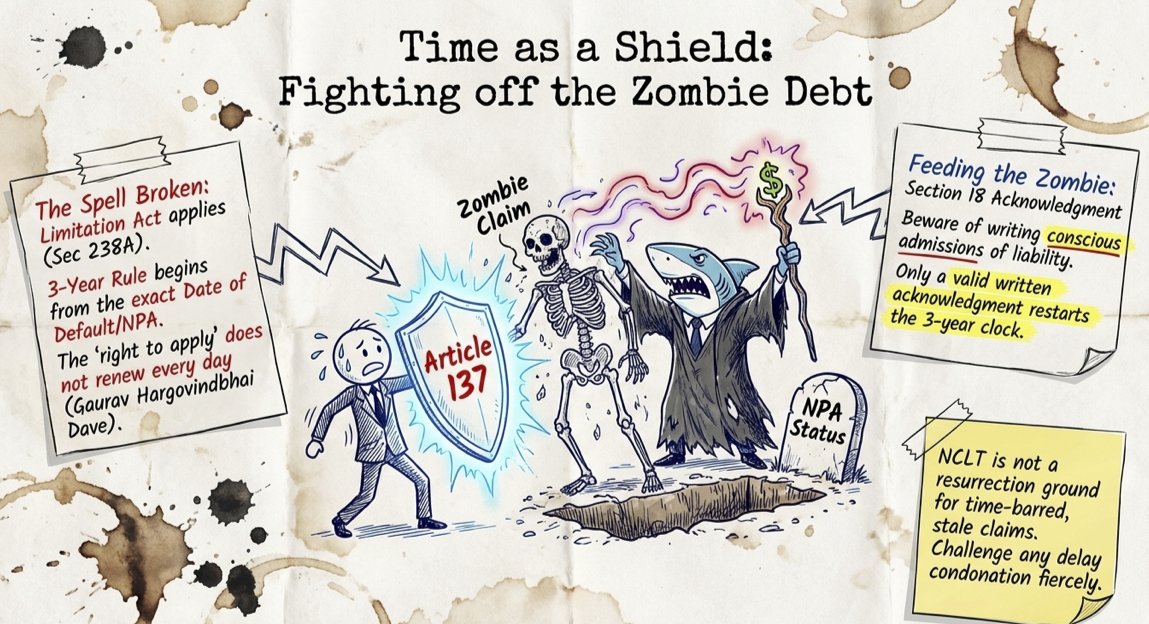

Time as a Shield: The Law of Limitation under IBC

The application of the Limitation Act, 1963, to the IBC was initially a point of contention until the insertion of Section 238A. The law is now settled: the provisions of the Limitation Act apply to proceedings under the IBC as far as may be.21 This provides corporate debtors with a robust defense against “stale claims” or age-old debts that creditors are attempting to resurrect through the insolvency forum.

Article 137 and the Three-Year Rule

Since Section 7 petitions are considered “applications” rather than “suits,” they fall under the residuary Article 137 of the Limitation Act, which prescribes a three-year period. The limitation begins to run from the “date of default”.21 In banking cases, this is often equated with the date the account was declared a Non-Performing Asset (NPA).21

A debtor can successfully argue for dismissal if:

- Lapse of Three Years: The petition was filed more than three years after the initial date of default/NPA declaration without any intervening events that extend the period.21

- No Continuous Default: The Supreme Court in Gaurav Hargovindbhai Dave clarified that the “right to apply” does not renew every day of a continuing default; it is fixed to the initial breach.21

- Invalid Acknowledgment: Under Section 18 of the Limitation Act, a fresh period of limitation begins if the debtor acknowledges the debt in writing before the expiration of the original period.21 Debtors can challenge these acknowledgments by arguing they were not “conscious” admissions of liability or were made under duress or as part of a settlement negotiation that failed.21

Extension and Condonation of Delay

While Section 5 of the Limitation Act allows for the condonation of delay if “sufficient cause” is shown, the judiciary has cautioned that the time-bound nature of the IBC necessitates a strict approach. Corporate debtors should aggressively challenge any attempt by a creditor to condone a delay of several years, arguing that the IBC is not a new lease of life for time-barred claims.21

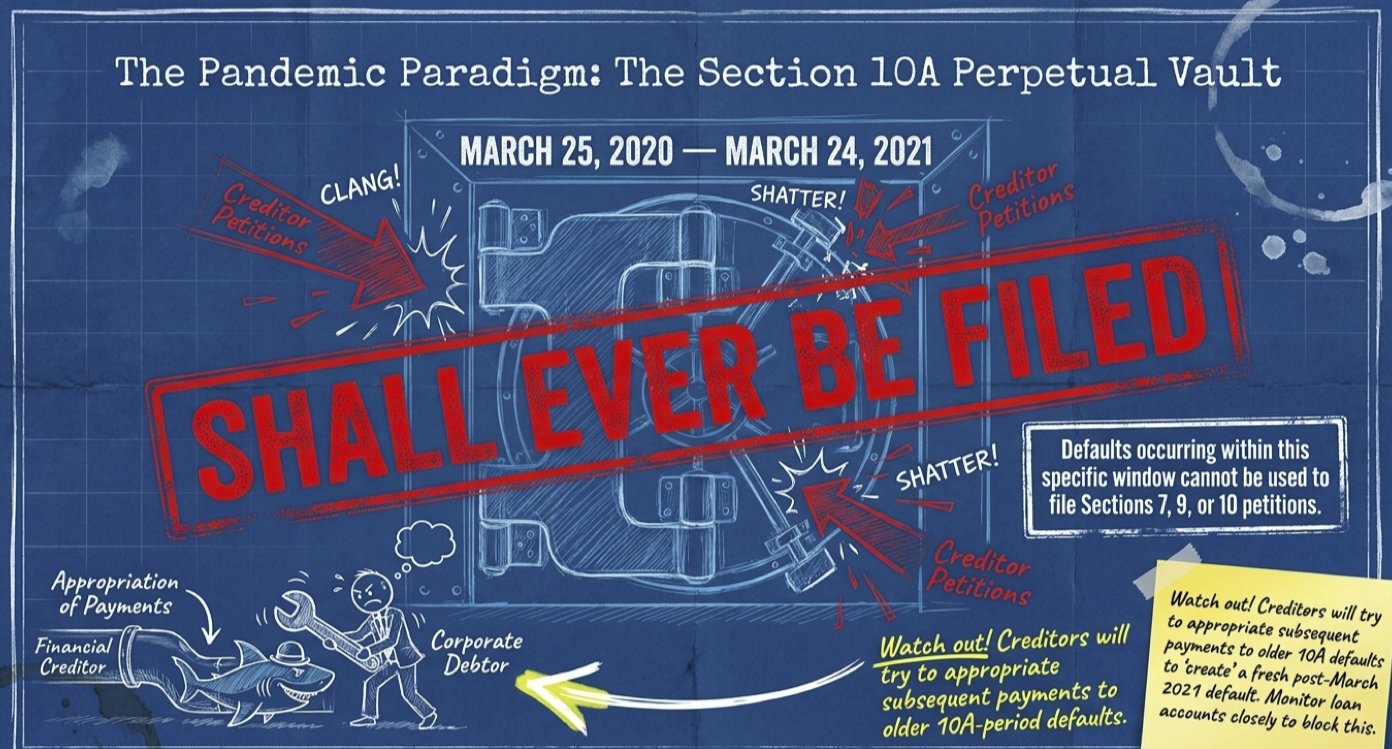

The Pandemic Paradigm: Section 10A and Perpetual Immunity

A unique defense arose during the COVID-19 pandemic with the introduction of Section 10A. This section suspended the filing of petitions under Sections 7, 9, and 10 for any default occurring between March 25, 2020, and March 24, 2021.28 The proviso to Section 10A is particularly powerful as it states that no application “shall ever be filed” for a default occurring during this period.28

For corporate debtors, this defense is an absolute bar. If a creditor identifies a default date that falls within this window, the petition must be dismissed in limine. This immunity is perpetual, meaning the creditor can never use that specific default as a ground for insolvency, even after the pandemic has subsided.28

However, creditors often attempt to circumvent this by:

- Arguing for Continuous Default: Claiming that since the default continued after March 2021, they can file a petition. The defense must counter this by citing the legislative intent to provide a “shield” for that specific period.29

- Appropriation of Payments: Attempting to adjust subsequent payments against older (10A period) defaults to “create” a fresh default post-March 2021. Debtors should monitor their loan accounts closely to ensure that payments are correctly appropriated to prevent such strategic maneuverings by lenders.28

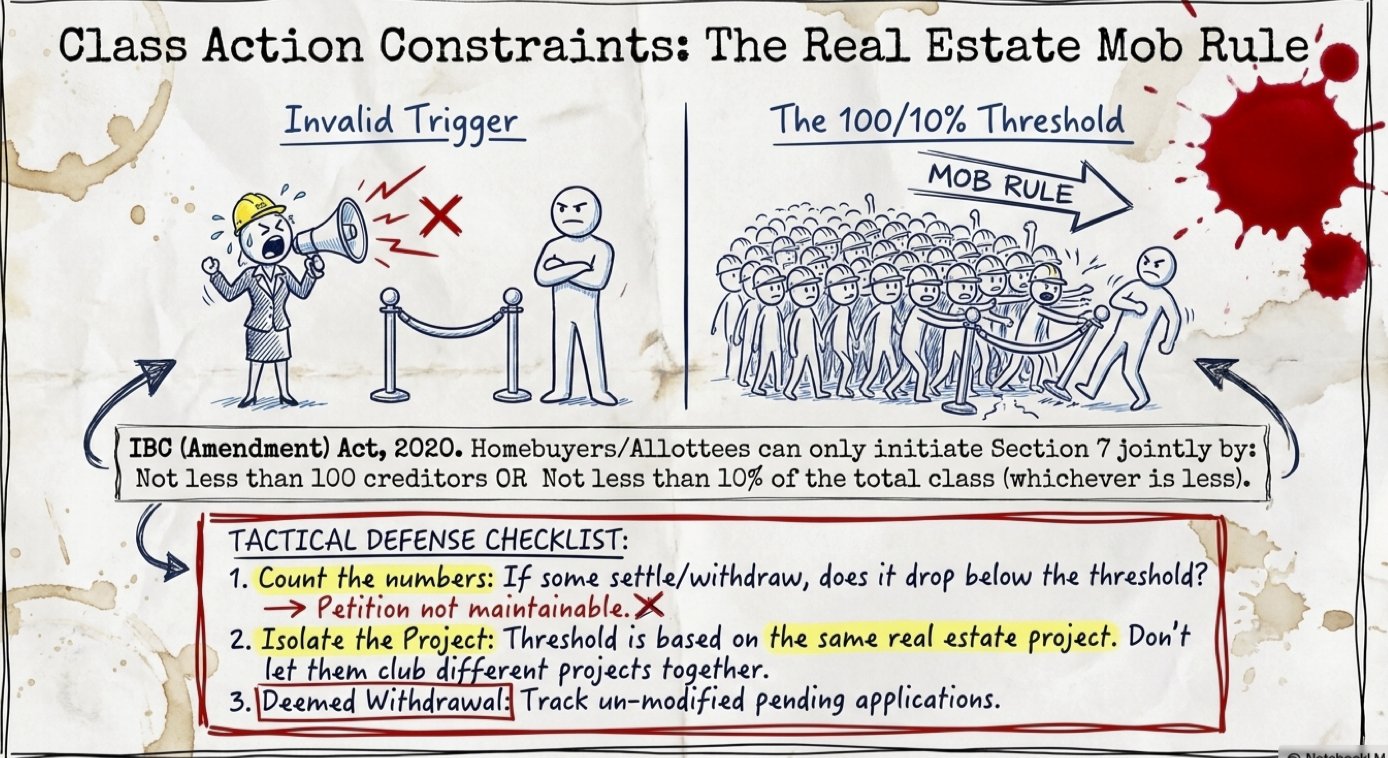

Class Action Constraints: Homebuyers and Allottee Thresholds

The status of homebuyers as “financial creditors” was a landmark development, but it also led to an explosion of litigation that threatened the stability of the real estate sector. In response, the IBC (Amendment) Act, 2020, introduced minimum thresholds for initiating CIRP by “creditors in a class”.31

The 100/10% Threshold

For homebuyers (allottees) or security holders (like bondholders), an application under Section 7 can only be filed jointly by not less than one hundred of such creditors or not less than ten percent of the total number of such creditors in the same class, whichever is less.31

Strategic defenses for real estate developers include:

- Threshold Failure: Challenging the maintainability of the petition if the number of petitioners falls below the threshold. If some petitioners withdraw or settle during the proceedings, the debtor can argue that the petition is no longer maintainable.33

- Project-wise Application: The threshold is calculated based on the “same real estate project.” Debtors can defend petitions by showing that the petitioners are from different projects and cannot be clubbed together to meet the numbers.6

- Deemed Withdrawal: Under the third proviso to Section 7(1), pending applications that did not meet the new threshold were required to be modified within thirty days, failing which they were “deemed to have been withdrawn”.33

This threshold ensures that the insolvency process is not triggered by a few disgruntled individuals but reflects a collective decision by a significant portion of the creditor class, thereby shielding developers from frivolous or avoidable applications.31

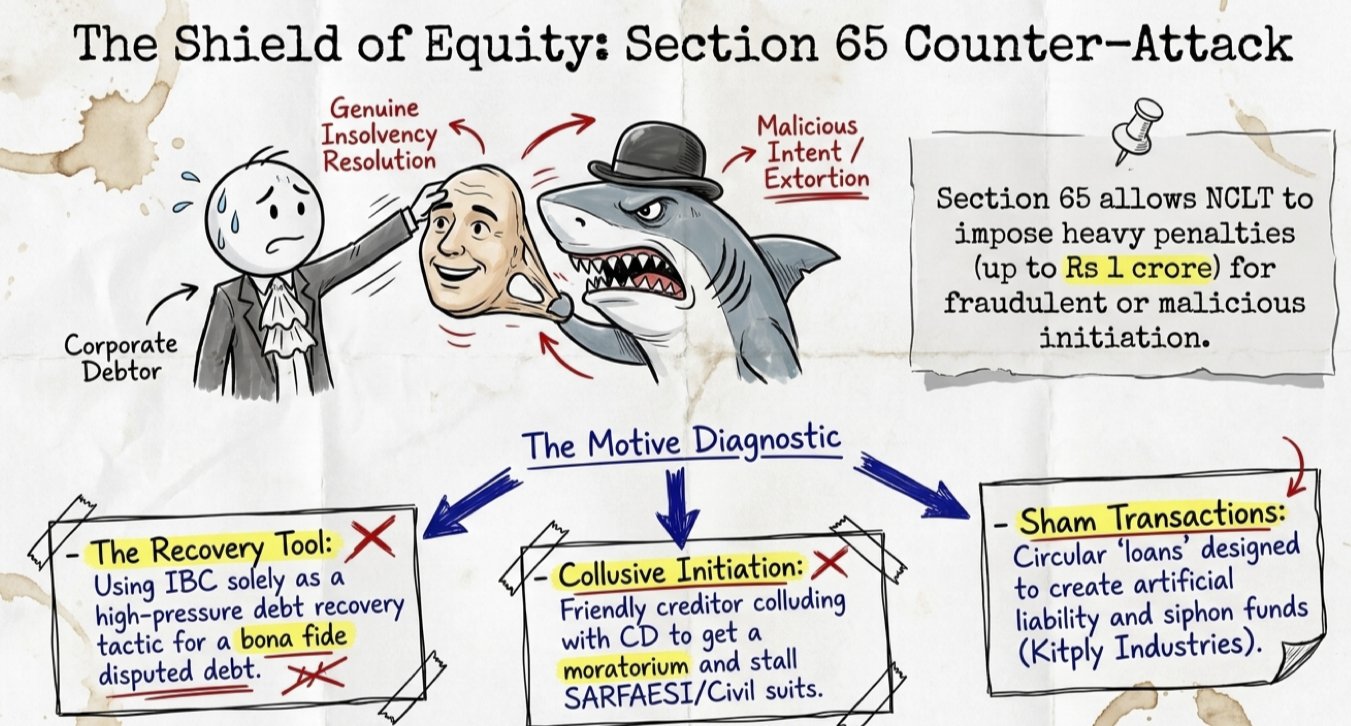

The Shield of Equity: Section 65 and Fraudulent Intent

Section 65 of the IBC is the “safety valve” of the insolvency framework. it provides for the imposition of penalties (ranging from ₹1 lakh to ₹1 crore) on any person who initiates the CIRP fraudulently or with malicious intent for any purpose other than the resolution of insolvency.36

Identifying Malice and Ulterior Motives

A corporate debtor can file an interlocutory application (IA) under Section 65 as a defense. The burden of proof is on the debtor to show that the petitioner’s intent was not the genuine resolution of the company’s stress.

Common grounds for a Section 65 defense include:

- Debt Recovery Tool: If the petition is clearly used as a pressure tactic to extract money from a solvent company, especially in a case where the debt is bona fide disputed.36

- Collusive Initiation: Cases where the debtor and a friendly creditor collude to trigger CIRP to obtain a moratorium and stall other recovery proceedings (like SARFAESI or a civil suit).40

- Sham and Circular Transactions: If the “loan” was part of a circular transaction designed to create an artificial liability for siphoning off funds. In the Kitply Industries case, workers successfully challenged a Section 7 petition by showing that the purported loans were circular transactions between related entities.39

The Supreme Court in Embassy Property Developments held that the NCLT and NCLAT have the jurisdiction to inquire into allegations of fraud, even if they involve complex factual determinations.40

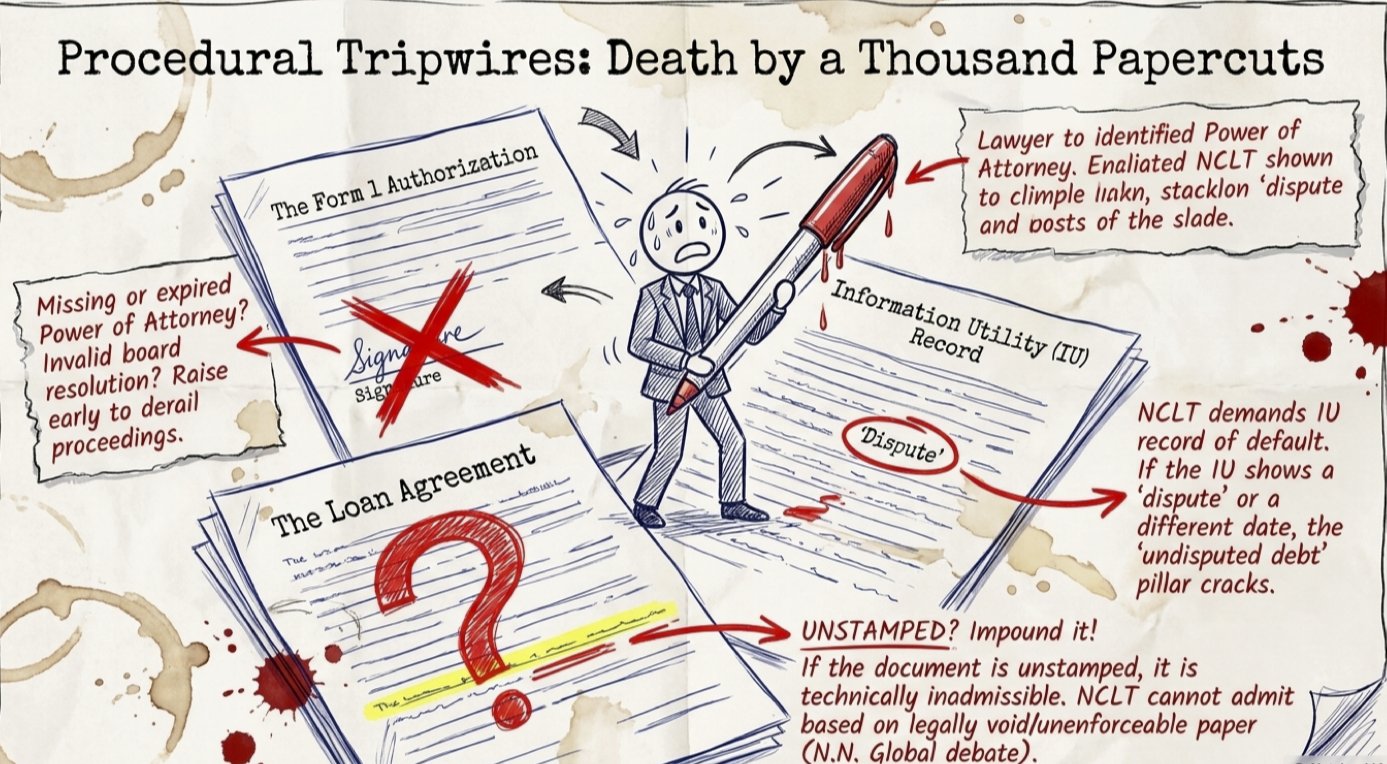

Procedural Rigor: Form 1, Rule 4, and Information Utilities

The IBC is a summary procedure where the Adjudicating Authority must follow a “tick-box” exercise for admission. Persistent procedural lapses by the financial creditor can provide the debtor with a technical but effective defense.

Non-Compliance with Form 1 and Authorization

The application must be in the prescribed Form 1 and must be accompanied by the record of default and the name of the proposed Resolution Professional.1

- Authorization Defects: The petition must be filed by a person “authorized” by the financial creditor. If the authorization (like a Power of Attorney or Board Resolution) is missing, expired, or invalid, the petition is liable to be dismissed. While the NCLAT has held that such defects are “curable,” the debtor should raise them early to delay or derail the proceedings.12

- Information Utility (IU) Discrepancies: While not yet mandatory for every bench, many NCLTs (especially the Principal Bench) now insist on a record-of-default from an IU. If the IU record shows a different date of default than the petition, or if it records a “dispute,” the debtor can argue that the Twin Test of “undisputed debt and default” is not met.16

The Conundrum of Unstamped Documents

A burgeoning area of defense involves the “validity” of the underlying financial documents. If a loan agreement or debenture trust deed is unstamped or insufficiently stamped, it is technically inadmissible in evidence under the Stamp Act.

- The Summary Nature Argument: Creditors often argue that Section 7 is a summary proceeding and the NCLT shouldn’t delve into stamping issues.44

- The Admissibility Argument: Debtors can argue that if the “existence of debt” is entirely dependent on an unstamped document, the document must be impounded. Post the N.N. Global judgment, the debate has intensified, with many arguing that the Adjudicating Authority cannot admit a petition based on a legally “void” or “unenforceable” document until the stamp duty deficiency is rectified.12

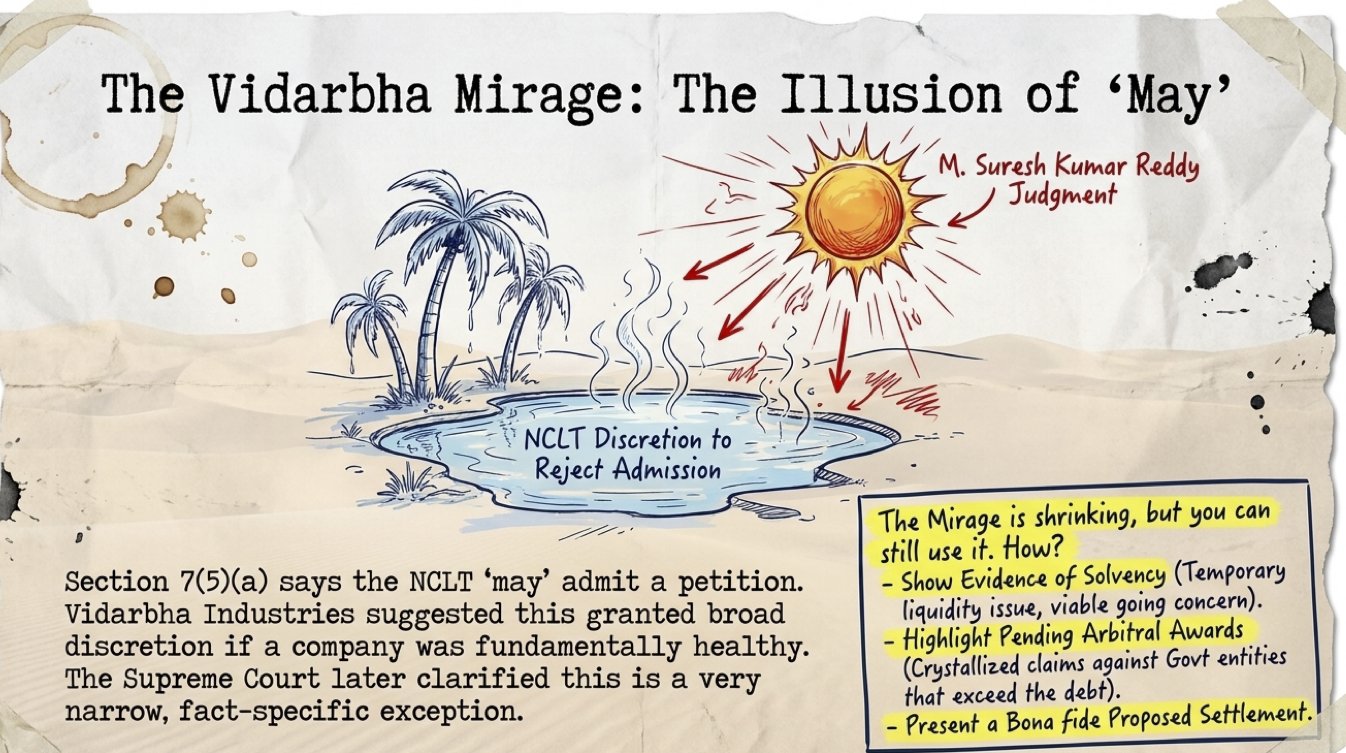

Judicial Discretion: The Vidarbha Exception and Beyond

The question of whether the word “may” in Section 7(5)(a) grants the NCLT discretion to refuse admission even if debt and default are proven is one of the most debated topics in Indian insolvency law.

The Rise and Fall of the Discretionary Doctrine

In Vidarbha Industries Power Ltd. v. Axis Bank Ltd., the Supreme Court observed that the NCLT “may” admit a petition, suggesting a level of discretion.9 The court held that if a company is fundamentally healthy and has realizable assets (such as a pending arbitral award) that exceed the debt, the NCLT should not blindly push it into insolvency.8

However, this was quickly clarified in M. Suresh Kumar Reddy v. Canara Bank, where the Court held that Vidarbha Industries was a “narrow, fact-specific exception”.8 The current legal position is that while the NCLT can examine the financial health of the debtor, it should not use this as a reason to deny admission once the jurisdictional facts of debt and default are proven, unless the circumstances are truly exceptional.8

Strategic Usage of the Vidarbha Argument

Corporate debtors can still use the Vidarbha rationale by presenting:

- Evidence of Solvency: Showing that the default was a temporary liquidity issue and the company is a viable going concern with sufficient cash flow to settle dues outside of CIRP.9

- Pending Arbitral Awards: If the debtor has a crystallized claim against a third party (especially a government entity) that could satisfy the creditor’s debt, this can be used to seek a stay on admission.9

- Proposed Settlement: Demonstrating that a bona fide settlement offer has been made which would protect the interest of the creditors better than an insolvency process.9

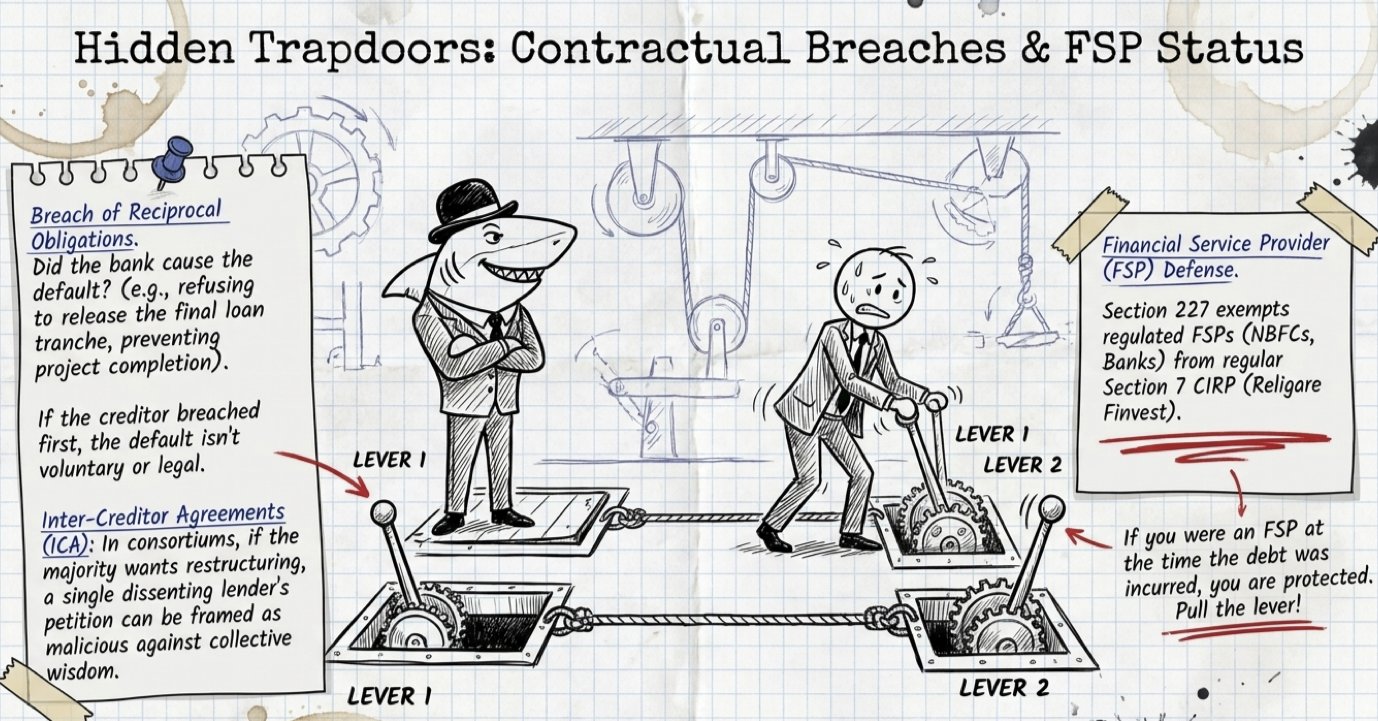

Contractual Interplay: Inter-Creditor Agreements and Loan Terms

A sophisticated defense often lies in the fine print of the financial contracts.

Breach of Reciprocal Obligations

If the default by the corporate debtor was caused by a prior breach of contract by the financial creditor, the debtor can argue that the “default” is not voluntary or legal. For example, if a bank refuses to release the final tranche of a construction loan, preventing the debtor from completing the project and generating revenue to repay the loan, the debtor can argue that the creditor is responsible for the trigger.43

Inter-Creditor Agreement (ICA) Dynamics

In consortium lending, the ICA governs the relationship between lenders. While the NCLT has held that the IBC overrides the ICA and an individual member’s right to file is not barred, a corporate debtor can still raise this as an equitable defense.43 If the majority of lenders (representing the “collective wisdom” of the CoC-to-be) believe the company should be restructured rather than put into CIRP, the debtor can argue that the petition of a single dissenting lender is malicious or counter-productive to the goals of the IBC.11

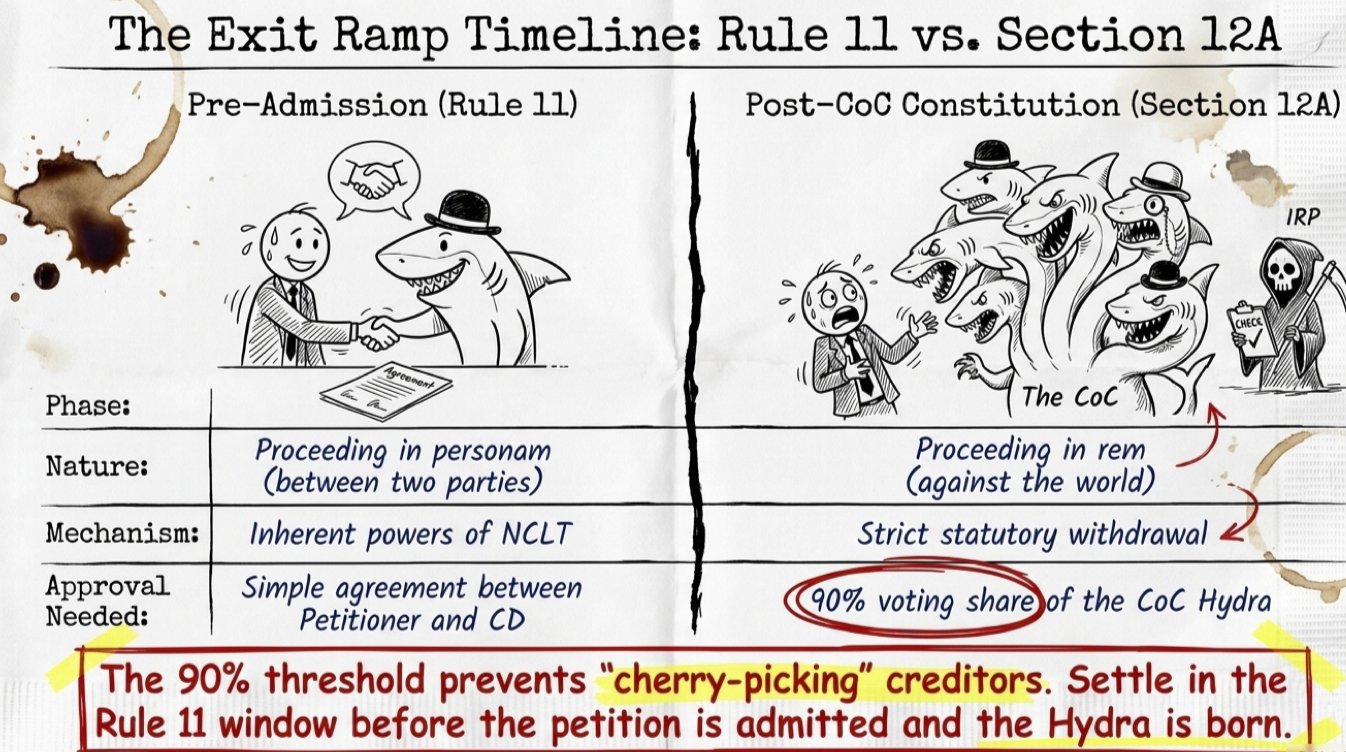

The Exit Ramp: Settlements and Withdrawal under Section 12A

The ultimate defense against a Section 7 petition is often a settlement. The IBC recognizes that the best resolution is one reached voluntarily between the parties.

Pre-Admission Settlement (Rule 11)

Before the petition is admitted, the NCLT has “inherent powers” under Rule 11 of the NCLT Rules, 2016, to allow the withdrawal of the petition if a settlement is reached. At this stage, no CoC approval is required.49 This is the most critical window for a corporate debtor to settle and prevent the “black mark” of an insolvency admission.

Post-Admission Settlement (Section 12A)

Once the petition is admitted, the case becomes a “proceeding in rem” (against the world) rather than a “proceeding in personam” (between two parties).51 Withdrawal under Section 12A then requires the approval of 90% of the voting share of the CoC.49

| Stage of Proceeding | Withdrawal Mechanism | Approval Required |

| Pre-Admission | Rule 11 of NCLT Rules | Agreement between Petitioner and CD |

| Post-Admission, Pre-CoC | Application by IRP (based on Swiss Ribbons & Sukhbeer Singh) | NCLT approval; notice to other claimants |

| Post-CoC Constitution | Section 12A of IBC | 90% voting share of the CoC |

| Post-Resolution Plan | Generally not permitted | Not applicable |

The 90% threshold is designed to ensure that the settlement is omnibus and involves all creditors, preventing the promoter from “cherry-picking” and settling with only a few vocal creditors while ignoring the rest.49

The Defense of the Financial Service Provider (FSP)

A significant but often overlooked defense is the classification of the debtor as a Financial Service Provider (FSP). Under Section 227 of the IBC, the central government has the power to notify specific classes of FSPs (like NBFCs or Banks) for which a separate insolvency regime applies.12

Corporate debtors can challenge a Section 7 petition by proving:

- Status as FSP: That they are engaged in the business of providing financial services and are regulated by an authority like the RBI or SEBI. In Religare Finvest Limited v. Strategic Credit Capital, the NCLAT ruled that CIRP cannot be initiated against an FSP under the general provisions of the IBC.12

- Relevant Date for FSP Status: There is ongoing judicial debate on whether the FSP status should be determined at the time of the transaction or the time of filing the petition. Debtors should argue that if they were an FSP at the time the debt was incurred, they should be protected from a “regular” Section 7 petition.12

Strategic Considerations for the Corporate Debtor’s Legal Team

Defending a Section 7 petition is a high-stakes chess game. The following tactical considerations are paramount:

- Early Engagement: The 14-day timeline for NCLT’s decision is often extended in practice, but the debtor must be ready with a comprehensive “Counter-Affidavit” immediately upon receipt of the notice.

- Projecting Solvency: Evidence of the company’s “going concern” status, such as tax filings, employee payroll records, and active project contracts, should be presented to the NCLT to show that insolvency is not the answer.1

- Cross-Referencing Claims: Meticulously checking the creditor’s calculations of interest and principal. Errors in the quantum of default can be used to show that the petition is “incomplete” or “misleading”.27

- Challenging the IRP’s Neutrality: If there is evidence that the proposed IRP has a conflict of interest or is facing disciplinary proceedings, this must be raised as a ground for rejection.1

Future Outlook and Conclusions

The jurisprudence surrounding Section 7 of the IBC is in a state of constant evolution. From the early “mandatory admission” stance of Innoventive, through the “discretionary window” of Vidarbha, and back to the “authoritative clarification” of M. Suresh Kumar Reddy, the law has sought a balance between creditor rights and debtor protection.

The analysis of the law points and landmark judgments suggests that the most successful defenses for corporate debtors are those that attack the jurisdictional facts (is it a financial debt? is there a default?) rather than those that appeal to equitable considerations. The “Twin Test” remains the primary battlefield, but the emergence of specialized defenses like Section 10A (pandemic immunity) and the strict 100/10% thresholds for real estate have provided debtors with a more diverse arsenal.

Furthermore, the rise of Section 65 as a deterrent against malicious petitions underscores the judiciary’s intent to prevent the IBC from being used as a tool for harassment or “recovery by other means.” For a corporate debtor, a holistic defense strategy must weave together technical procedural objections, statutory bars of limitation and immunity, and a deep-dive into the commercial substance of the financial transaction. In the final analysis, the defense of a Section 7 petition is not just about avoiding insolvency; it is about ensuring that the potent medicine of the IBC is only administered to those truly in need of a terminal resolution, while protecting viable enterprises from premature or wrongful corporate death.

Works cited

- Section 7 of IBC – Insolvency and Bankruptcy Code – Tranzission, accessed on April 29, 2026, https://tranzission.in/section-7-of-ibc-insolvency-and-bankruptcy-code/

- CIRP Under IBC: Complete Guide to Initiation, Sections 7, 9, 10 & 95–100 and Post-Admission Process – Anirudh Associates, accessed on April 29, 2026, https://anirudhassociates.com/cirp-under-ibc-complete-guide-to-initiation-sections-7-9-10-95-100/

- Fundamentals of IBC: Financial Creditor v. Operational Creditor, accessed on April 29, 2026, https://www.pslchambers.com/wp-content/uploads/2020/04/Fundamentals-of-IBC-Financial-Creditor-v.-Operational-Creditor.pdf

- Section 5(8) of IBC: A Detailed Overview on Financial Debt in IBC – The Legal School, accessed on April 29, 2026, https://thelegalschool.in/blog/section-5-8-ibc

- ‘FINANCIAL DEBT’ UNDER INSOLVENCY AND BANKRUPTCY ACT, 2016 | TaxTMI, accessed on April 29, 2026, https://www.taxtmi.com/article/detailed?id=14918

- IBC Section 7-Initiation of corporate insolvency resolution process by financial creditor., accessed on April 29, 2026, https://ca2013.com/section-7-initiation-corporate-insolvency-resolution-process-financial-creditor/

- Section 7 of IBC – Insolvency and Bankruptcy Code, 2016 : Initiation of corporate insolvency resolution process (CIRP) by financial creditor – IBC Laws, accessed on April 29, 2026, https://ibclaw.in/section-7-initiation-of-corporate-insolvency-resolution-process-by-financial-creditor-chapter-ii-corporate-insolvency-resolution-processcirp-part-ii-insolvency-resolution-and-liquidation-for-corpor/

- Supreme Court: Admission of Insolvency Petition (IBC) is mandatory …, accessed on April 29, 2026, https://ibclaw.in/supreme-court-admission-of-insolvency-petition-ibc-is-mandatory-vidarbha-industries-judgment-is-an-exception/

- Vidarbha Industries v. Axis Bank – Top Ranked Legal, accessed on April 29, 2026, https://www.toprankedlegal.com/vidarbha-industries-v-axis-bank/

- IN THE NATIONAL COMPANY LAW TRIBUNAL DIVISION BENCH, COURT NO. II KOLKATA I.A. (IB) No. 1324/(KB)/2022 In Company Petition (IB), accessed on April 29, 2026, https://nclt.gov.in/gen_pdf.php?filepath=/Efile_Document/ncltdoc/casedoc/1908134046082022/04/Order-Challenge/04_order-Challange_004_1704199753101797288265940649a824f.pdf

- Mandatory Admission of Section 7 Application: A Step in the Wrong Direction? – The Competition and Commercial Law Review, accessed on April 29, 2026, https://www.tcclr.com/post/mandatory-admission-of-section-7-application-a-step-in-the-wrong-direction

- NCLAT Fortnightly: Important orders on IBC (Feb 1 – Feb 15, 2026), accessed on April 29, 2026, https://www.barandbench.com/columns/nclat-fortnightly-important-orders-on-ibc-feb-1-feb-15-2026

- Recharacterization of Debt under IBC: Party Autonomy vs …, accessed on April 29, 2026, https://elplaw.in/leadership/recharacterization-of-debt-under-ibc-party-autonomy-vs-regulatory-safeguards-in-the-context-of-financial-vs-operational-debt-2/

- Understanding Financial and Operational Debt Under IBC – Mahendra Bhavsar & Co., accessed on April 29, 2026, https://mahendrabhavsar.com/financial-vs-operational-debt-under-ibc-explained/

- Anuj Jain vs. Axis Bank : Whither Banks? – Taxmann, accessed on April 29, 2026, https://www.taxmann.com/research/fema-banking-insurance/top-story/105010000000018039/anuj-jain-vs-axis-bank-whither-banks-experts-opinion

- When there is a record of dispute in the Information Utility (IU), the Adjudicating Authority (NCLT) is obliged to reject an application filed under Section 9 of the IBC – Bhuvan Kumar Gupta Vs. Maverick Developers and Colonisers Pvt. Ltd. and Anr. – NCLAT New Delhi, accessed on April 29, 2026, https://ibclaw.in/bhuvan-kumar-gupta-vs-maverick-developers-and-colonisers-pvt-ltd-and-anr-nclat-new-delhi/

- Preferential Transactions under IBC- Anuj Jain v. Axis Bank Ltd and others – White Code Legal, accessed on April 29, 2026, https://whitecode.legal/more/OTEw/Preferential-Transactions-under-IBC-Anuj-Jain-v-Axis-Bank-Ltd-and-others

- Anuj Jain, Interim R… v. Axis Bank Limited An… | Supreme Court Of India | Judgment – CaseMine, accessed on April 29, 2026, https://www.casemine.com/judgement/in/634e5b4c4b8a8b31d4f3c2ef

- Anuj Jain (RP) v. Axis Bank Limited & Ors. – PSL Advocates and Solicitors, accessed on April 29, 2026, https://www.pslchambers.com/case-brief/anuj-jain-interim-resolution-professional-for-jaypee-infratech-ltd-v-axis-bank-limited-ors/

- Summary of Supreme Court judgment in Anuj Jain Interim Resolution Professional for Jaypee Infratech Limited Vs. Axis Bank Limited etc. – IBC Laws, accessed on April 29, 2026, https://ibclaw.in/anuj-jain-interim-resolution-professional-for-jaypee-infratech-limited-vs-axis-bank-limited-etc-supreme-court-2/

- Analysis provisions of Limitation Act, 1963 with respect to Insolvency …, accessed on April 29, 2026, https://ibclaw.in/analysis-of-the-provisions-of-limitation-act-1963-with-respect-to-insolvency-and-bankruptcy-code-2016/

- IBC barred by limitation or not | Article – Chambers and Partners, accessed on April 29, 2026, https://chambers.com/articles/ibc-barred-by-limitation-or-not

- IBC S 238A Limitation We see no reason why Section 14 or 18 of the Limitation Act, 1963 should not apply to proceeding – PLRonline.in – PLR, accessed on April 29, 2026, https://supremecourtonline.in/ibc-s-238a-limitation-we-see-no-reason-why-section-14-or-18-of-the-limitation-act-1963-should-not-apply-to-proceeding-under-section-7-or-section-9-of-the-ibc-section-238a-of-the-ibc-make/?hilite=feed%2F%2F%2F%2F&pdf=15767

- Cases on Section 7 Ibc Application Denials, accessed on April 29, 2026, https://supremetoday.ai/search/cases-on-section-7-ibc-application-denials

- LIMITATION IN INSOLVENCY PROCEEDINGS – VALIDITY OF BOOK ENTRIES ? | TaxTMI, accessed on April 29, 2026, https://www.taxtmi.com/article/detailed?id=15258

- Applicability of Limitation Act to the Insolvency and Bankruptcy Code: Enactments, Interpretations, – NLS Forum, accessed on April 29, 2026, https://forum.nls.ac.in/nlsblr-blog-post/applicability-of-limitation-act-to-the-insolvency-and-bankruptcy-code-enactments-interpretations/

- IN THE NATIONAL COMPANY LAW TRIBUNAL AMARAVATI BENCH (Through Hybrid Mode) Item No.1 IA (IBC)/418/2024, IA (IBC)/98/2025 in CP – LiveLaw, accessed on April 29, 2026, https://www.livelaw.in/pdf_upload/ms-canara-bank-versus-ms-vasavi-power-services-pvt-ltd-614963.pdf

- Covid-19: Insolvency and Bankruptcy Code amended to suspend initiation of insolvency proceedings for six months – Trilegal, accessed on April 29, 2026, https://trilegal.com/knowledge_repository/covid-19-insolvency-and-bankruptcy-code-amended-to-suspend-initiation-of-insolvency-proceedings-for-six-months/

- division bench i, chennai – cp/ib/157/che/2021 – NCLT, accessed on April 29, 2026, https://nclt.gov.in/gen_pdf.php?filepath=/Efile_Document/ncltdoc/casedoc/3305118032812021/04/Order-Challenge/04_order-Challange_004_16506970422282917136263a3525663d.pdf

- Impact of Section 10A of the IBC: Relief or Roadblock? – Samisti legal, accessed on April 29, 2026, https://samistilegal.in/impact-of-section-10a-of-the-ibc-relief-or-roadblock/

- 100 homebuyers’ nod must for IBC – Synergy Insolvency Professionals LLP, accessed on April 29, 2026, https://synergyinsolvency.com/100-homebuyers-nod-must-for-ibc-against-realtor-supreme-court/

- Homebuyers as Financial Creditors under the IBC: Judicial Evolution, Thresholds, and Equity in Insolvency Resolution – B&B Associates LLP, accessed on April 29, 2026, https://bnblegal.com/article/homebuyers-as-financial-creditors-under-ibc/

- Rights of homebuyers in the ever-changing Indian insolvency regime – AZB & Partners, accessed on April 29, 2026, https://www.azbpartners.com/bank/rights-of-homebuyers-in-the-ever-changing-indian-insolvency-regime/

- In event allottees, fails to comply with the second Proviso to Section 7(1) of IBC, to modify the application within 30 days, deeming provision of law shall come into play and the CIRP application u/s 7 shall be deemed to have been withdrawn – Hari Om Dixit Vs. Ajit Srivastava and Ors. – NCLAT New Delhi – IBC Laws, accessed on April 29, 2026, https://ibclaw.in/hari-om-dixit-vs-ajit-srivastava-and-ors-nclat-new-delhi/

- IN THE NATIONAL COMPANY LAW TRIBUNAL PRINCIPAL BENCH, NEW DELHI CP (IB) – 350 (PB)/2021 IA-946/2023 ORDER UNDER SECTION 7 OF T, accessed on April 29, 2026, https://nclt.gov.in/gen_pdf.php?filepath=/Efile_Document/ncltdoc/casedoc/0710102064972021/04/Order-Challenge/04_order-Challange_004_167999767516844221106422baeb034fe.pdf

- Fraudulent or Malicious Initiation of Insolvency Proceedings under …, accessed on April 29, 2026, https://ibclaw.in/fraudulent-or-malicious-initiation-of-insolvency-proceedings-under-the-insolvency-and-bankruptcy-code-2016-jurisprudence-of-section-65-of-the-code-by-adv-r-sruthi/

- Section 65 – India Code, accessed on April 29, 2026, https://www.indiacode.nic.in/show-data?actid=AC_CEN_2_11_00055_201631_1517807328273§ionId=844§ionno=65&orderno=87

- Section 65 of IBC: Fraudulent or Malicious Initiation of Insolvency Proceedings, accessed on April 29, 2026, https://thelegalschool.in/blog/section-65-ibc

- Fraud Or Malicious Intent U/S 65 Of IBC Is Proven If Terms Of Loan Extended By Financial Creditor Are Designed To Cause Default: NCLT – LiveLawBiz, accessed on April 29, 2026, https://www.livelawbiz.com/amp/ibc-cases/fraud-or-malicious-intent-us-65-of-ibc-is-proven-if-terms-of-loan-extended-by-financial-creditor-are-designed-to-cause-default-nclt-289768

- Fraudulent Initiation of Insolvency Resolution Process – K Law, accessed on April 29, 2026, https://www.klaw.in/fraudulent-initiation-of-insolvency-resolution-process-3/

- NATIONAL COMPANY LAW APPELLATE TRIBUNAL, PRINCIPAL BENCH, NEW DELHI, accessed on April 29, 2026, https://nclat.nic.in/display-board/view_order_pdf?fid=9910110085022024&&l=delhi&&d=2025-03-07&&order_type=J

- J U D G M E N T – Nclat, accessed on April 29, 2026, https://nclat.nic.in/display-board/view_order_pdf?fid=9910134053932025&&l=delhi&&d=2025-08-25&&order_type=J

- The Inter-Creditor Agreement is a contractual arrangement and …, accessed on April 29, 2026, https://ibclaw.in/state-bank-of-india-vs-madhucon-toll-highways-ltd-nclt-hyderabad-bench/

- IBC Section 7 proceedings: The conundrum of unstamped …, accessed on April 29, 2026, https://nlujlawreview.in/insolvency-and-bankruptcy-law/ibc-section-7-proceedings-the-conundrum-of-unstamped-documents/

- Case Analysis on Vidarbha Industries Power Ltd. Vs. Axis Bank Ltd. – By Adv. Nitika Rawat, accessed on April 29, 2026, https://ibclaw.blog/case-analysis-on-vidarbha-industries-power-ltd-vs-axis-bank-ltd-by-adv-nitika-rawat/

- Mandatory Section 7 Admission Reaffirmed: NCLAT – Fox Mandal, accessed on April 29, 2026, https://foxmandal.in/News/mandatory-section-7-admission-reaffirmed-nclat/

- Course Correction – The Vidarbha judgment clarified | Dispute Resolution Blog, accessed on April 29, 2026, https://disputeresolution.cyrilamarchandblogs.com/2023/08/course-correction-the-vidarbha-judgment-clarified/

- Inter-creditor agreement among consortium can’t come in way of CIRP plea by one member if debt and default is proved – Taxmann, accessed on April 29, 2026, https://www.taxmann.com/research/ibc/top-story/101010000000192389/inter-creditor-agreement-among-consortium-cant-come-in-way-of-cirp-plea-by-one-member-if-debt-and-default-is-proved-caselaws

- CoC Approval under Section 12A of the IBC A Stumbling Block to Settlement – Tranzission, accessed on April 29, 2026, https://tranzission.in/coc-approval-under-section-12a-of-the-ibc/

- 12A CIRP Withdrawal can’t be postponed until CoC Constituted, accessed on April 29, 2026, https://carajput.com/blog/12a-cirp-withdrawal/

- IN THE NATIONAL COMPANY LAW TRIBUNAL MUMBAI BENCH-IV IA No. 2209/2021 Under Section 12A of Insolvency & Bankruptcy Code, 201, accessed on April 29, 2026, https://nclt.gov.in/gen_pdf.php?filepath=/Efile_Document/ncltdoc/casedoc/2709138061102022/04/Order-Challenge/04_order-Challange_004_1679316041488628613641854492d652.pdf

- Section 12A withdrawal prior to constitution of CoC: A smooth exit or legal quagmire – By Adv. Amir Bavani and Adv. Rishika Kumar, AB Legal – IBC Laws, accessed on April 29, 2026, https://ibclaw.in/section-12a-withdrawal-prior-to-constitution-of-coc-a-smooth-exit-or-legal-quagmire/

- Section 12A and its significant impact on CIRP Process – iiipicai, accessed on April 29, 2026, https://www.iiipicai.in/wp-content/uploads/2025/01/35-39-Article.pdf