Defending Against Section 14 CJM/ DM Physical Possession notice of Property under SARFAESI and DRT Stay order

Creditor and contributor of this article:

Patra’s Law Chambers:

About Us:

Patra’s Law Chambers is a law firm with offices in Kolkata & Delhi, offering comprehensive legal services across various domains. Established in 2020 by Advocate Sudip Patra (Advocate, Supreme Court of India & Calcutta High Court) an alumnus of the Prestigious Rajiv Gandhi School of Intellectual Property Law, IIT Kharagpur ,with Post Graduate diploma in Business Law from IIM Calcutta, the firm specializes in Civil, Criminal, Writs,High Court Matters, Trademark, Copyright, Company, Tax, Banking, Property disputes, Service law, Family law, and Supreme Court matters.You can know more about us in here

Kolkata Office:

NICCO HOUSE, 6th Floor, 2, Hare Street, Kolkata-700001 (Near Calcutta High Court)

Delhi Office:

House no: 4455/5, First Floor, Ward No. XV, Gali Shahid

Bhagat Singh, Main Bazar Road, Paharganj, New Delhi-110055

Website: www.patraslawchambers.com

Email: [email protected]

Phone: +91 890 222 4444/ +91 7003 715 325

View this post on Instagram

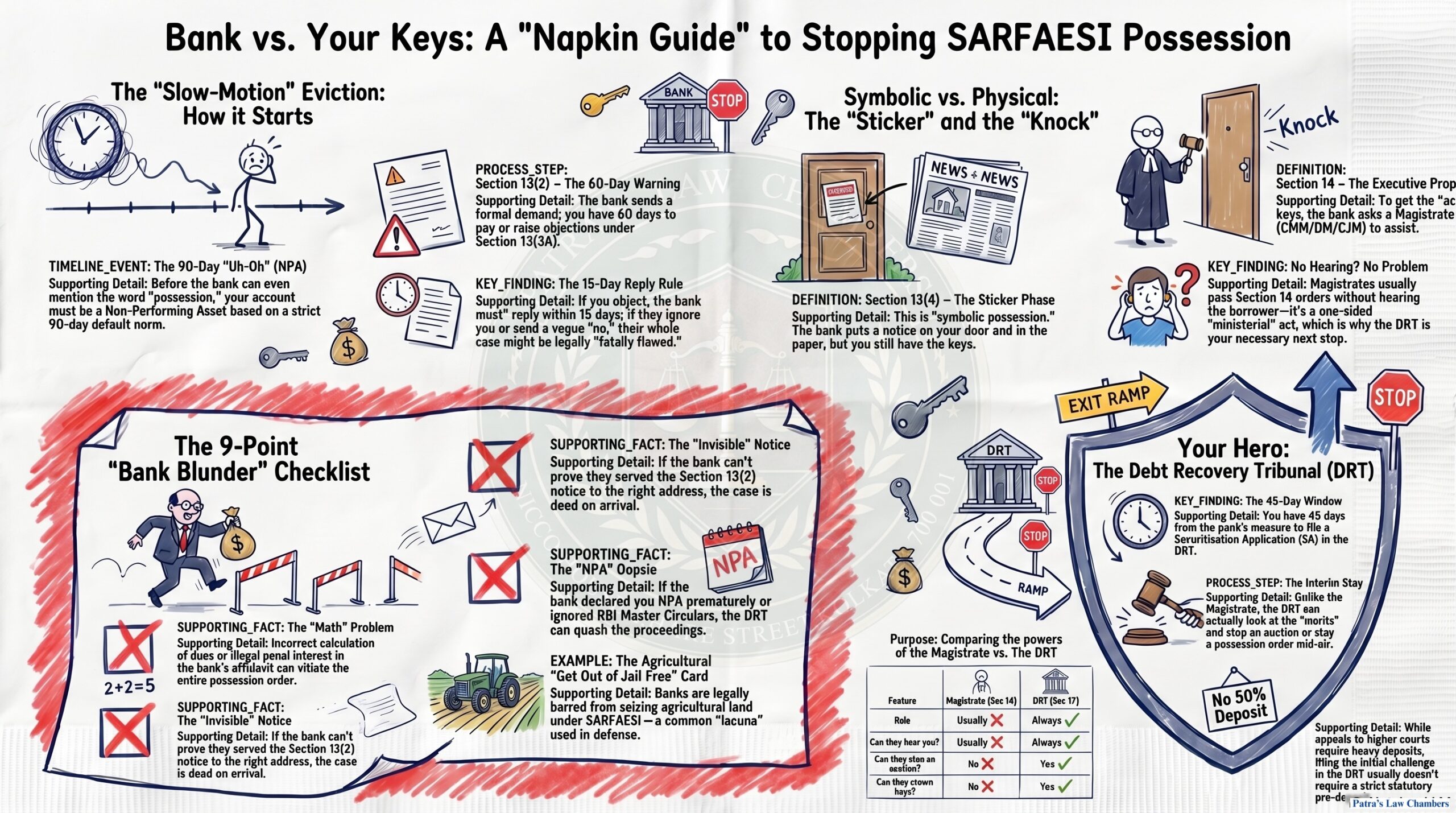

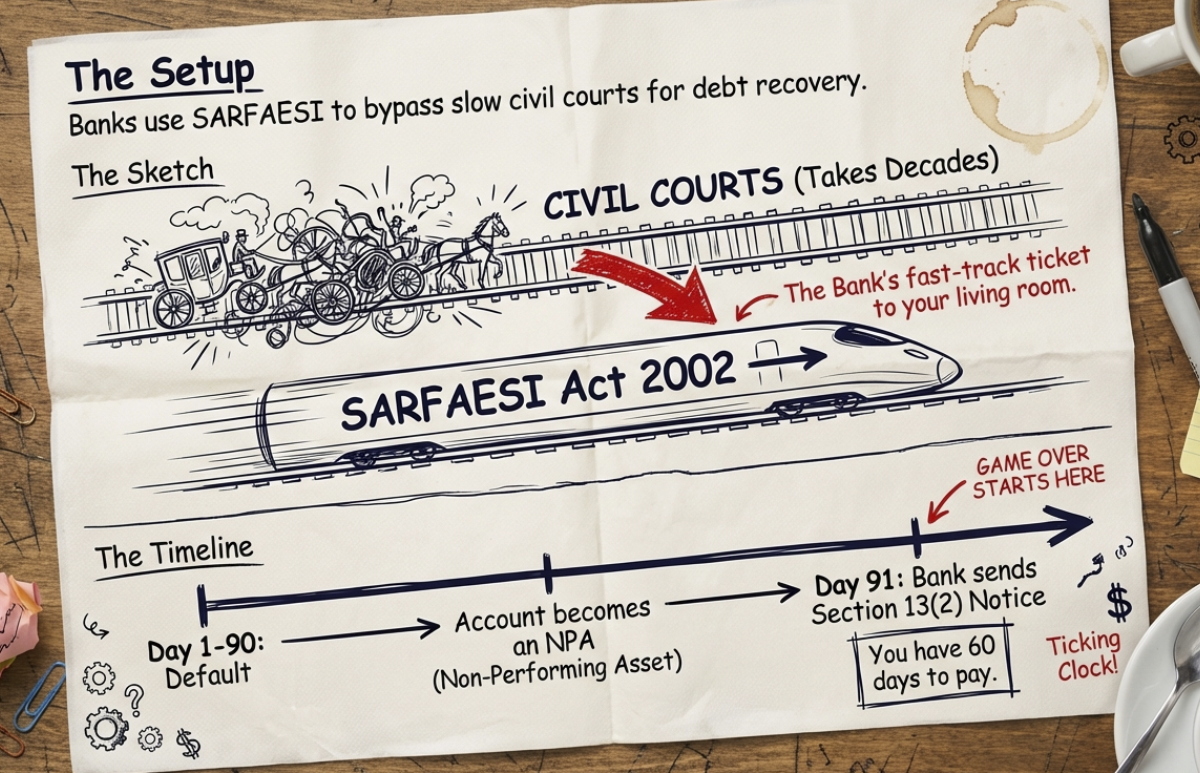

The enforcement of security interests in the Indian banking sector is governed primarily by the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002. This legislation provides a fast-track mechanism for banks to recover dues by bypassing the traditionally slow civil court system.1 Central to this recovery framework is the transition from a demand for payment to the actual physical takeover of secured assets. While Section 13(4) grants the creditor the power to take possession, the practical execution often requires the “executive prop” provided by Section 14.3 This section empowers the Chief Metropolitan Magistrate (CMM), the District Magistrate (DM), or the Chief Judicial Magistrate (CJM) to assist the creditor in obtaining physical possession.5 However, this power is not absolute, and the statutory architecture provides a robust system of checks and balances through the Debt Recovery Tribunal (DRT) under Section 17.7

The Statutory Architecture of Enforcement Under Sections 13 and 14

The recovery process begins with the classification of the borrower’s account as a Non-Performing Asset (NPA) based on specific 90-day default norms established by the Reserve Bank of India.9 Following this, the creditor must issue a demand notice under Section 13(2), allowing the borrower 60 days to discharge their liabilities.1 If the borrower submits a representation or objection under Section 13(3A), the creditor is legally obligated to consider it and, if rejecting it, communicate the reasons within 15 days.5

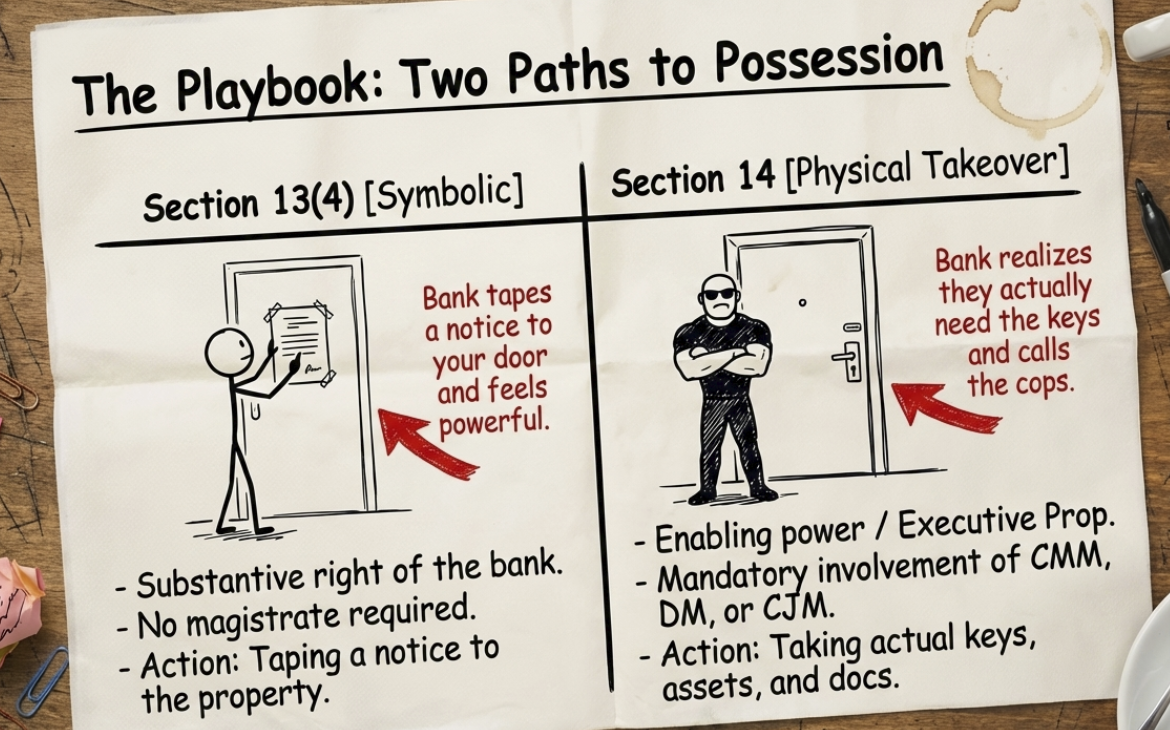

When the 60-day period expires without repayment, the creditor is entitled to take measures under Section 13(4). These measures include taking “symbolic possession,” which involves the affixation of a possession notice and its publication in newspapers.5 To achieve “actual physical possession,” the creditor must often invoke Section 14.3

The Distinctions Between Section 13(4) and Section 14

| Feature | Section 13(4) Measures | Section 14 Assistance |

| Nature of Power | Substantive right to take possession.3 | Enabling power to provide executive assistance.3 |

| Intervention | No magistrate intervention required for symbolic steps.2 | Mandatory involvement of CMM, DM, or CJM for physical takeover.3 |

| Target | Can include management takeover or appointing a manager.1 | Strictly limited to taking possession of assets and documents.3 |

| Prerequisites | Expiry of 60-day notice and 13(3A) compliance.2 | Valid Section 13(2) notice and filing of a 9-point affidavit.6 |

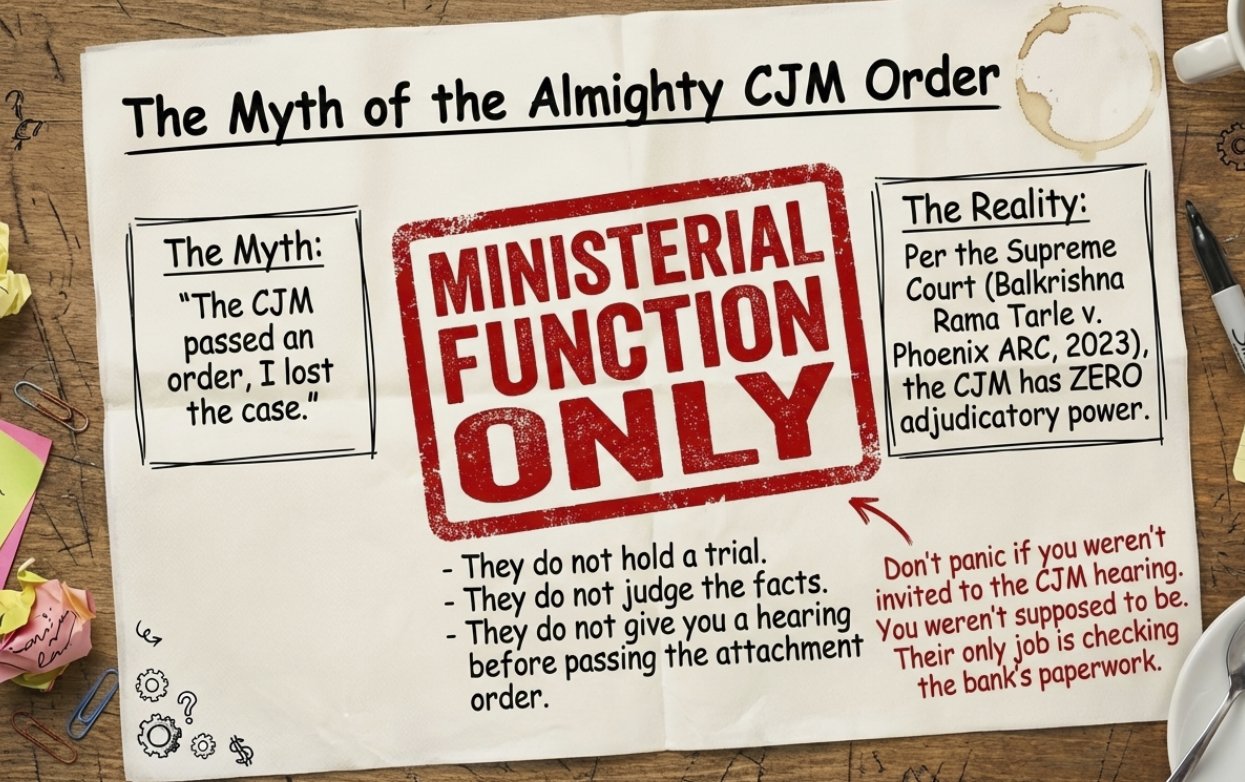

| Adjudication | Actions challenged post-facto in the DRT.2 | Magistrate performs a ministerial function with no adjudicatory power.12 |

The Ambit and Power of the Petitioner Before the DRT

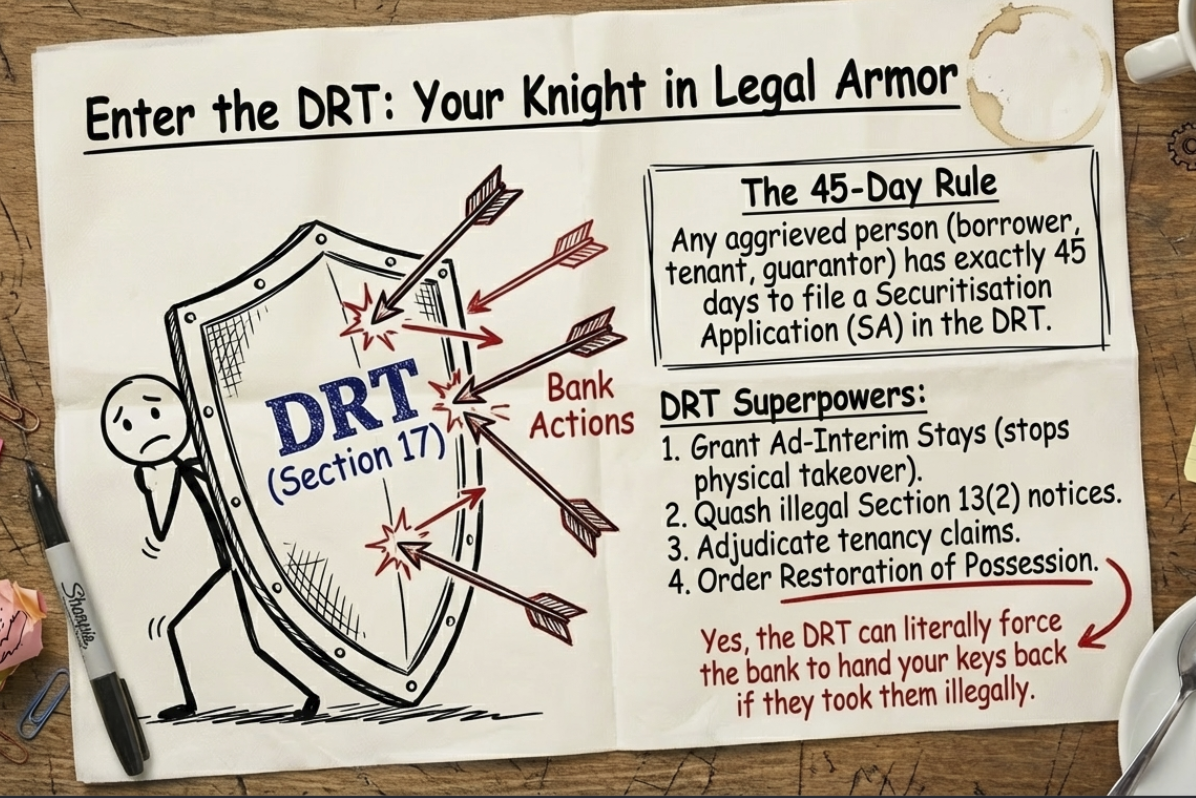

Any person aggrieved by the measures taken by a secured creditor under Section 13(4) has the right to approach the Debt Recovery Tribunal under Section 17.2 This includes the borrower, a guarantor, or even a third party (such as a tenant or a co-owner).7 The petitioner’s primary remedy is to file a Securitisation Application (SA) within 45 days of the measure being taken.2

The Power of the DRT to Grant Stay Orders

The DRT’s jurisdiction allows it to examine not just the procedural adherence of the bank but also the factual legality of the debt.15 The tribunal has the power to:

- Grant Ad-Interim Stays: If the petitioner demonstrates a prima facie case, the DRT can stay the possession proceedings or an auction.10

- Order Restoration of Possession: If physical possession was taken following a flawed CJM order, the DRT can restore that possession to the borrower.2

- Quash Illegal Notices: The DRT can set aside notices issued in violation of the Act or RBI guidelines.10

- Adjudicate Tenancy Claims: The DRT is specifically empowered to determine the validity of leasehold or tenancy rights.2

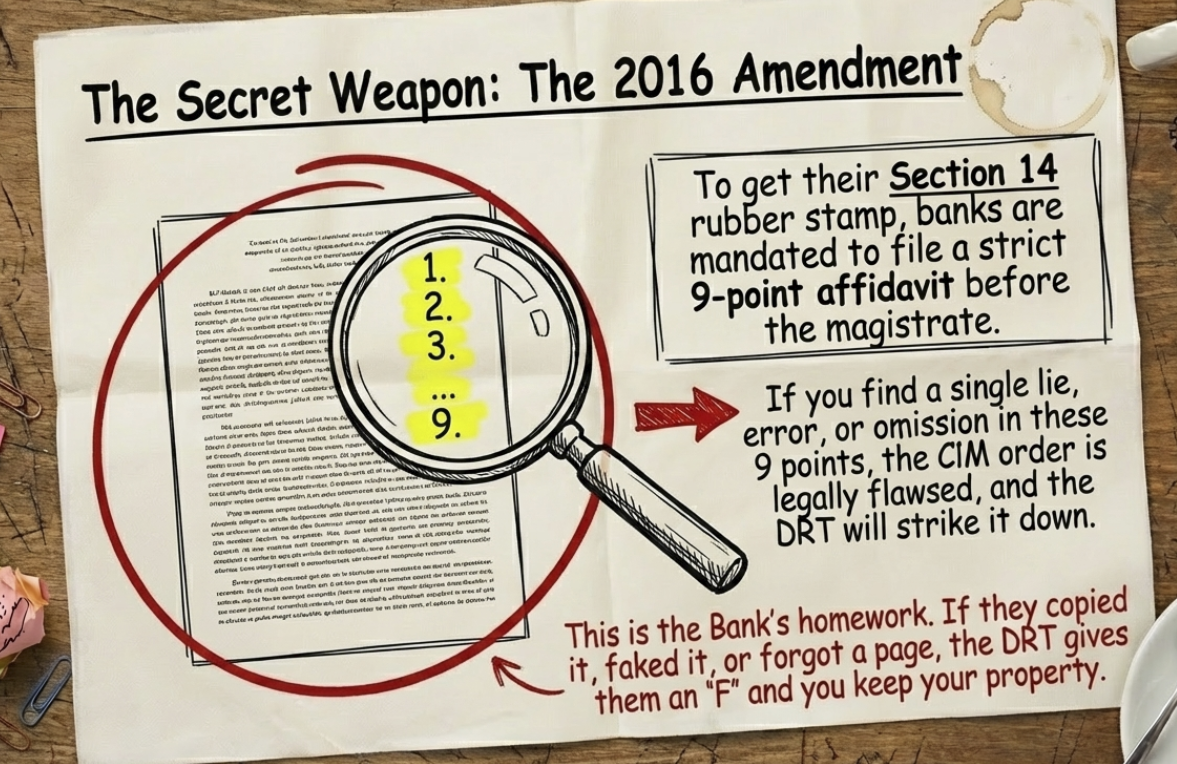

Lacunas and Grounds for Challenging CJM Orders in the DRT

The legality of a Section 14 order is predicated on the strict fulfillment of requirements set out in the first proviso to Section 14(1).6 The 2016 amendment made it mandatory for the secured creditor to file an affidavit declaring nine specific points.4

The 9-Point Affidavit Analysis and Defensive Grounds

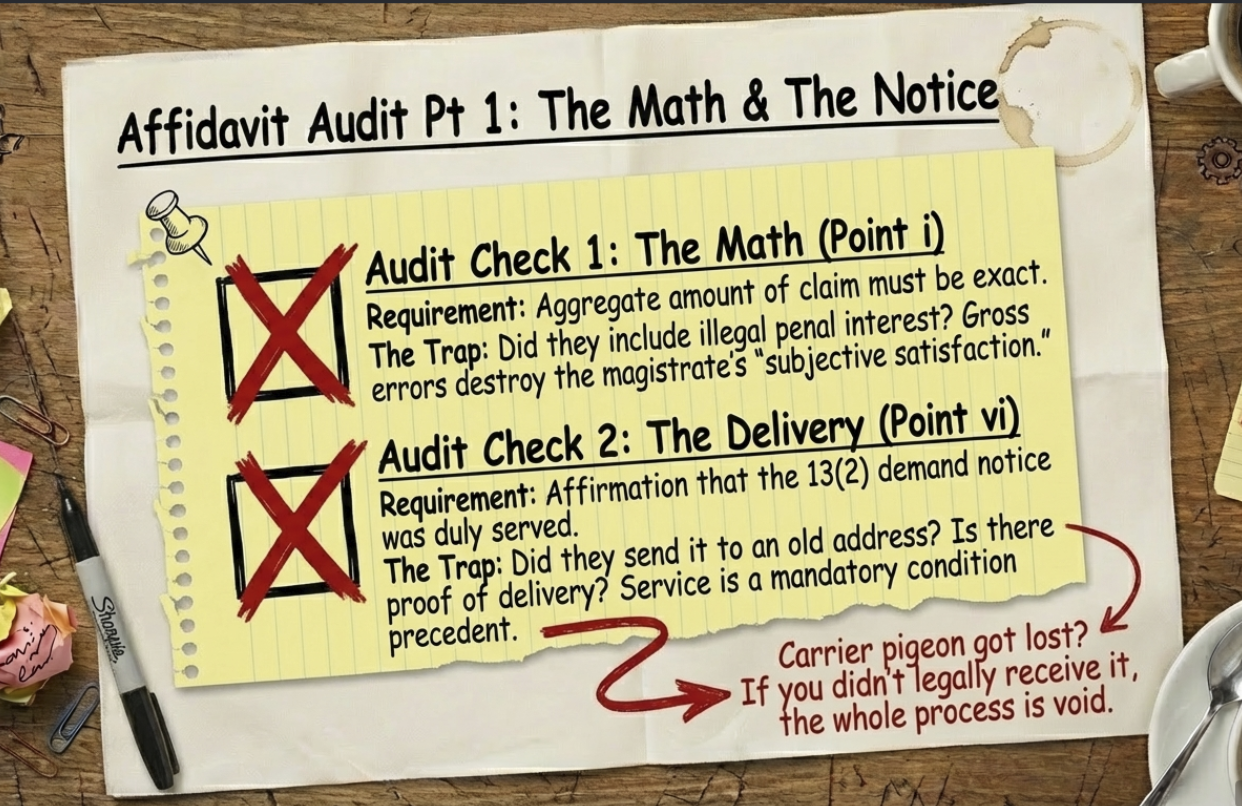

| Affidavit Requirement | Potential Lacuna for Defense | Legal Implication |

| (i) Aggregate amount of total claim as on the filing date. | Incorrect calculation of dues; inclusion of illegal penal interest. | Gross errors vitiate the “subjective satisfaction” of the Magistrate. |

| (ii) Valid and subsisting security interest within limitation. | Expiry of limitation period or defective mortgage deed. | A claim barred by limitation cannot be enforced via SARFAESI. |

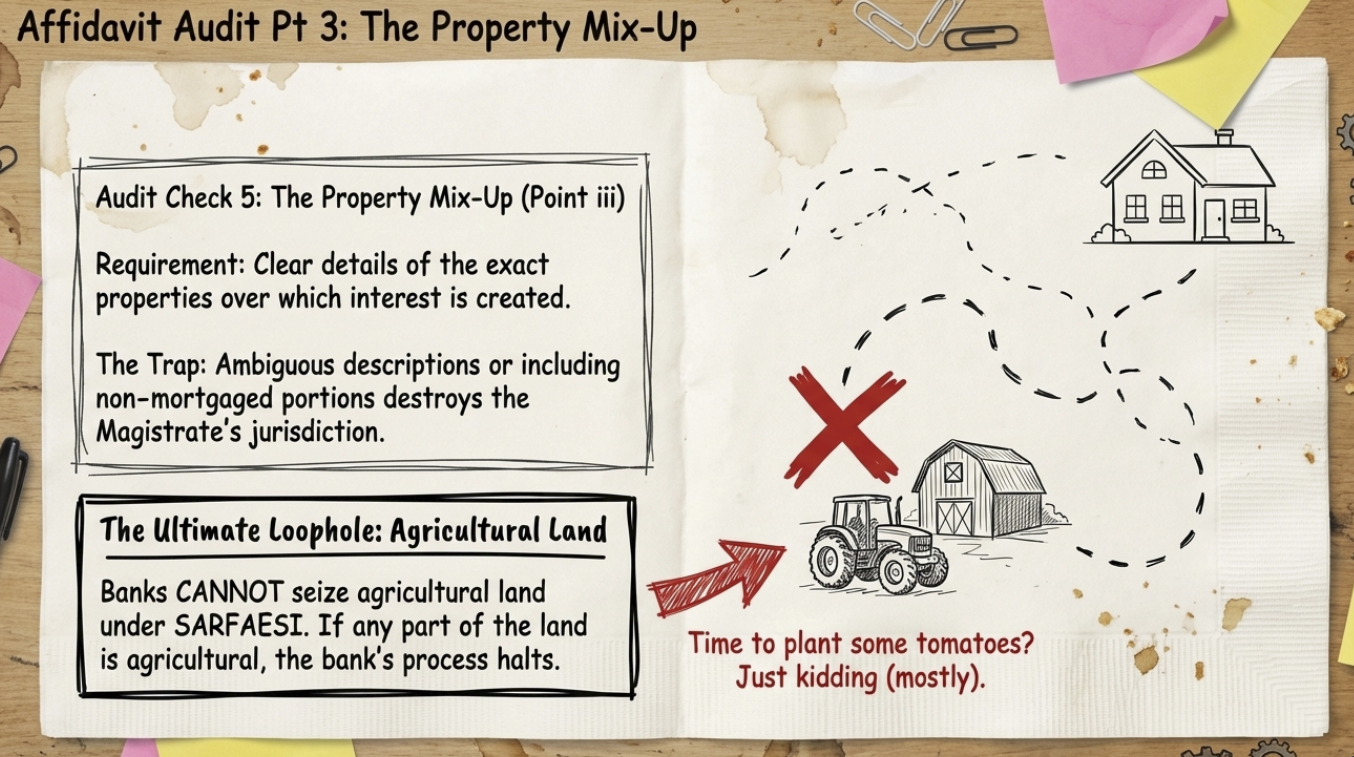

| (iii) Clear details of the properties over which the interest is created. | Ambiguous property description or inclusion of non-mortgaged portions. | Prevails over the Magistrate’s jurisdiction to order possession. |

| (iv) Affirmation that the borrower has committed a default. | Bank’s failure to credit payments or disputed schedules. | No default means no jurisdiction to invoke Section 13 or 14. |

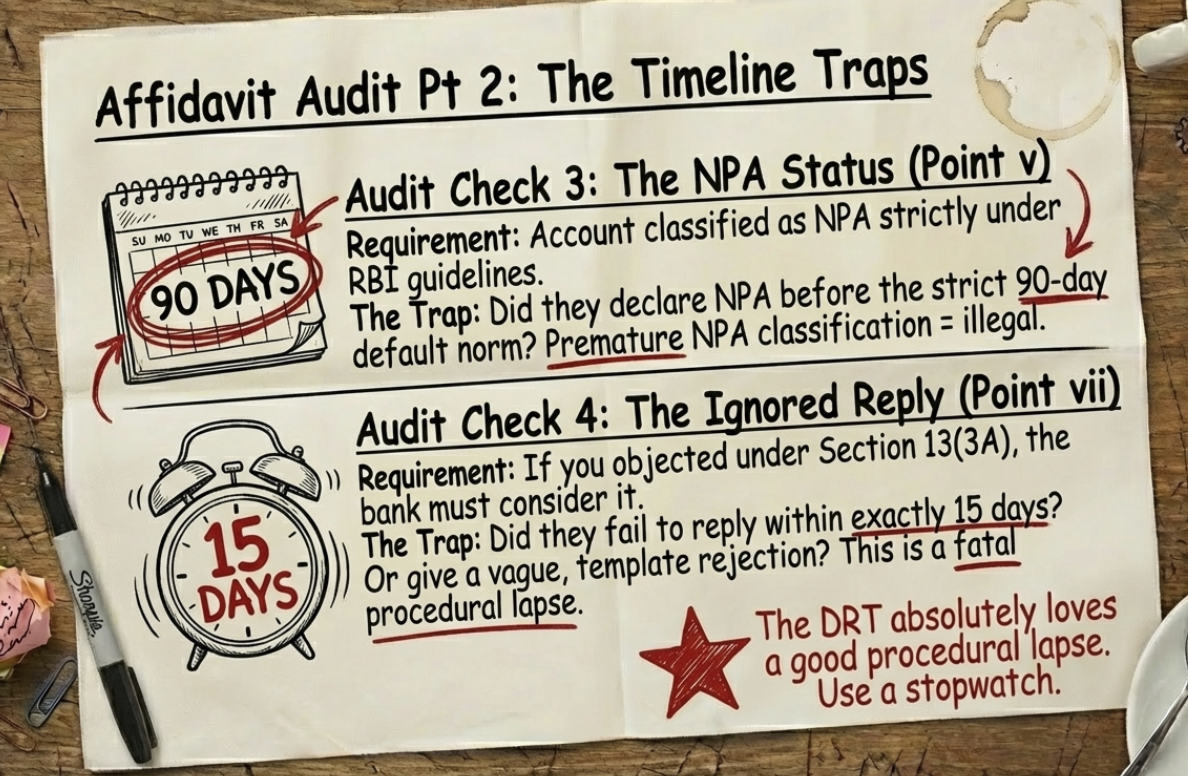

| (v) Classification of the account as an NPA under RBI guidelines. | Premature NPA declaration or failure to follow RBI Master Circulars. | Illegal NPA classification voids all subsequent actions. |

| (vi) Affirmation that the 13(2) notice was duly served. | Notice sent to wrong address or lack of proof of delivery. | Service is a mandatory condition precedent for recovery.18 |

| (vii) Consideration and communication of reasons for 13(3A) rejection. | Failure to reply within 15 days or providing a vague rejection. | Non-compliance is a fatal procedural lapse.11 |

| (viii) Entitlement to take possession under Section 13(4) and 14. | Failure to complete symbolic steps or incorrect legal interpretation. | Bank must establish its legal right before seeking assistance. |

| (ix) Affirmation of compliance with the Act and SI Rules, 2002. | General failure to adhere to statutory timelines or notification rules. | A blanket declaration challengeable by specific Rule violations.19 |

Landmark Judgments and Their Practical Implications

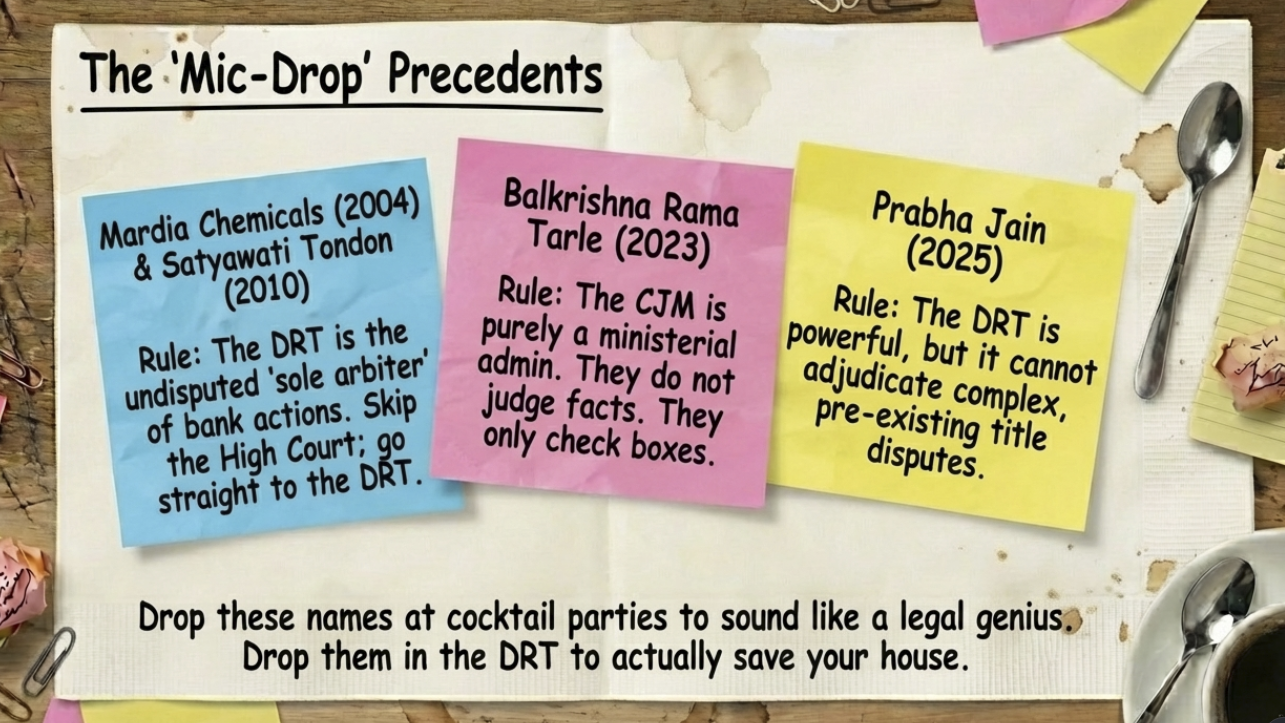

- Mardia Chemicals Ltd. v. Union of India (2004): Established the DRT as the primary forum where the merits of a bank’s actions can be scrutinized.2

- United Bank of India v. Satyawati Tondon (2010): Solidified the DRT as the “sole arbiter” of SARFAESI disputes, cautioning High Courts against entertaining Writ Petitions when an alternative remedy exists.7

- Harshad Govardhan Sondagar v. IARC Ltd. (2014): Protected the rights of bona fide tenants, leading to the 2016 amendment empowering the DRT to adjudicate tenancy disputes.14

- Balkrishna Rama Tarle v. Phoenix ARC (2023): Reaffirmed the CJM/DM’s role as “ministerial” once procedural affidavit requirements are met.13

- Central Bank of India v. Smt. Prabha Jain (2025): Clarified that the DRT cannot adjudicate complex title disputes between the borrower and a third party that existed before the mortgage was created .

Frequently Asked Questions (FAQs) on Section 14 and DRT Stays

Q1: Can the DRT really stop a CJM order if it is labeled “final” in Section 14(3)?

Yes. While Section 14(3) protects the Magistrate’s action from being questioned in a civil court, the DRT has the power under Section 17 to examine the underlying “measures” taken by the bank . If the bank’s affidavit was false or if the 13(2) notice was never served, the DRT can stay the physical takeover or even order the restoration of possession .

Q2: I was never given a hearing before the CJM passed the attachment order. Is this legal?

Yes, it is legal. The Supreme Court has clarified that Section 14 proceedings are ministerial and do not require a hearing or notice to the borrower before the order is passed . However, this “one-sided” nature is exactly why you have the right to approach the DRT immediately after the order is passed to challenge the bank’s claims .

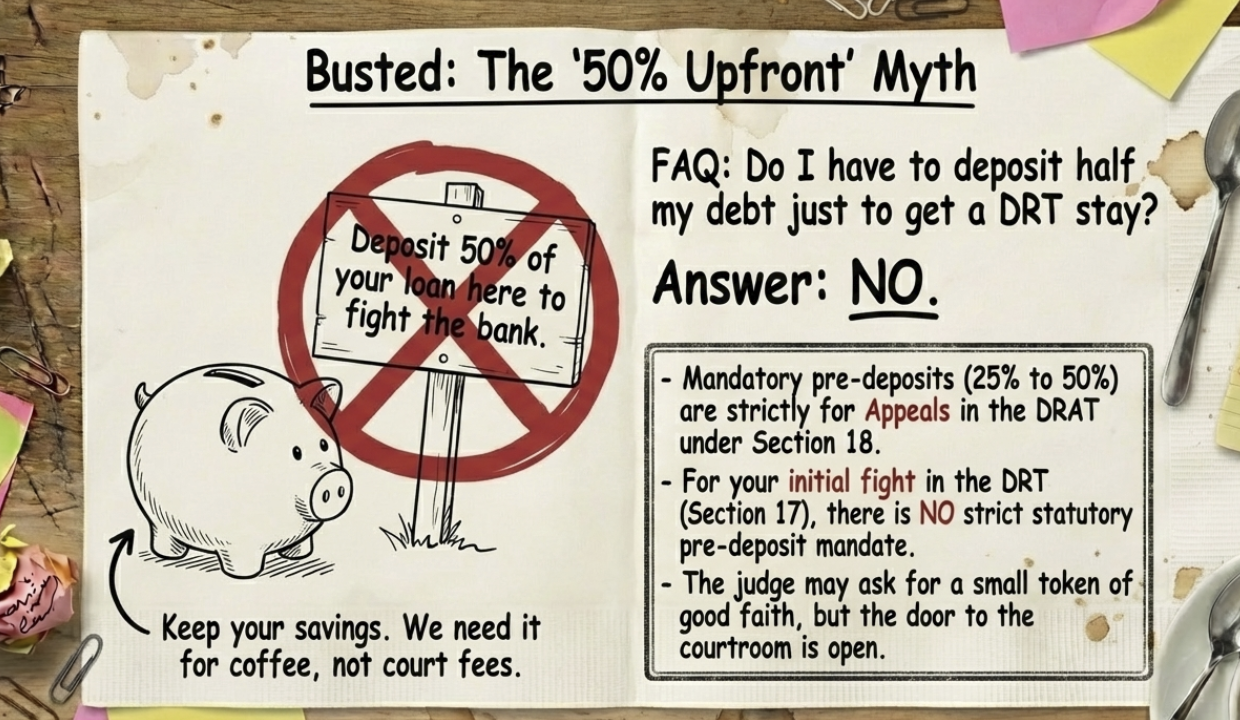

Q3: Is a pre-deposit of 50% of the debt mandatory to get a stay from the DRT?

No. The mandatory pre-deposit (usually 25% to 50%) is required for filing an appeal before the Debt Recovery Appellate Tribunal (DRAT) under Section 18 . For an initial application in the DRT under Section 17, there is no strict statutory pre-deposit, although the DRT may impose conditions (like depositing a small portion of the dues) as a requirement for granting a stay .

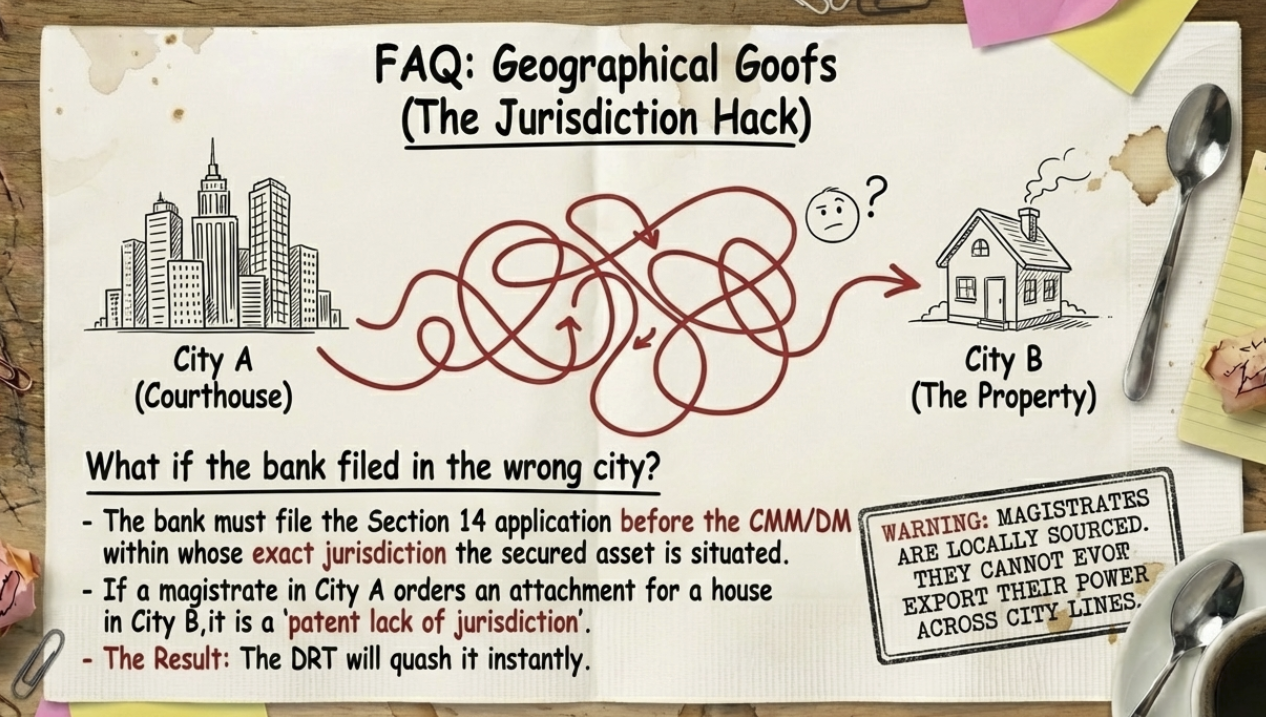

Q4: What if the property is in a different city than where the bank filed the application? This is a major jurisdictional lacuna. The bank must file the Section 14 application before the CMM or DM within whose jurisdiction the secured asset is situated.23 If a CJM in City A passes an order for a property in City B, that order is a “patent lack of jurisdiction” and can be quashed by the DRT.4

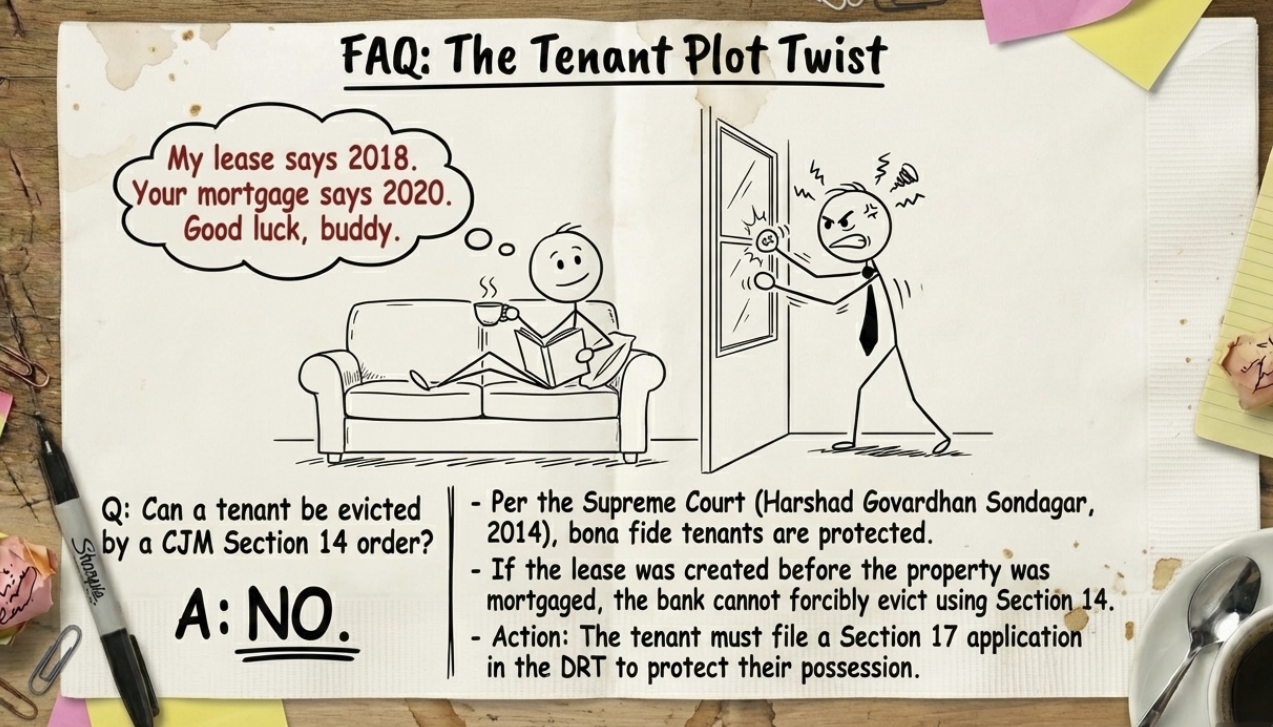

Q5: Can a tenant who has been living in the property for 5 years be evicted by a Section 14 order? If the lease was created before the property was mortgaged, the tenant is protected.14 The bank cannot use Section 14 to forcibly evict a lawful tenant whose lease is valid . The tenant should immediately file an application under Section 17 to protect their possession.11

The “Secret” to Stopping a CJM Order

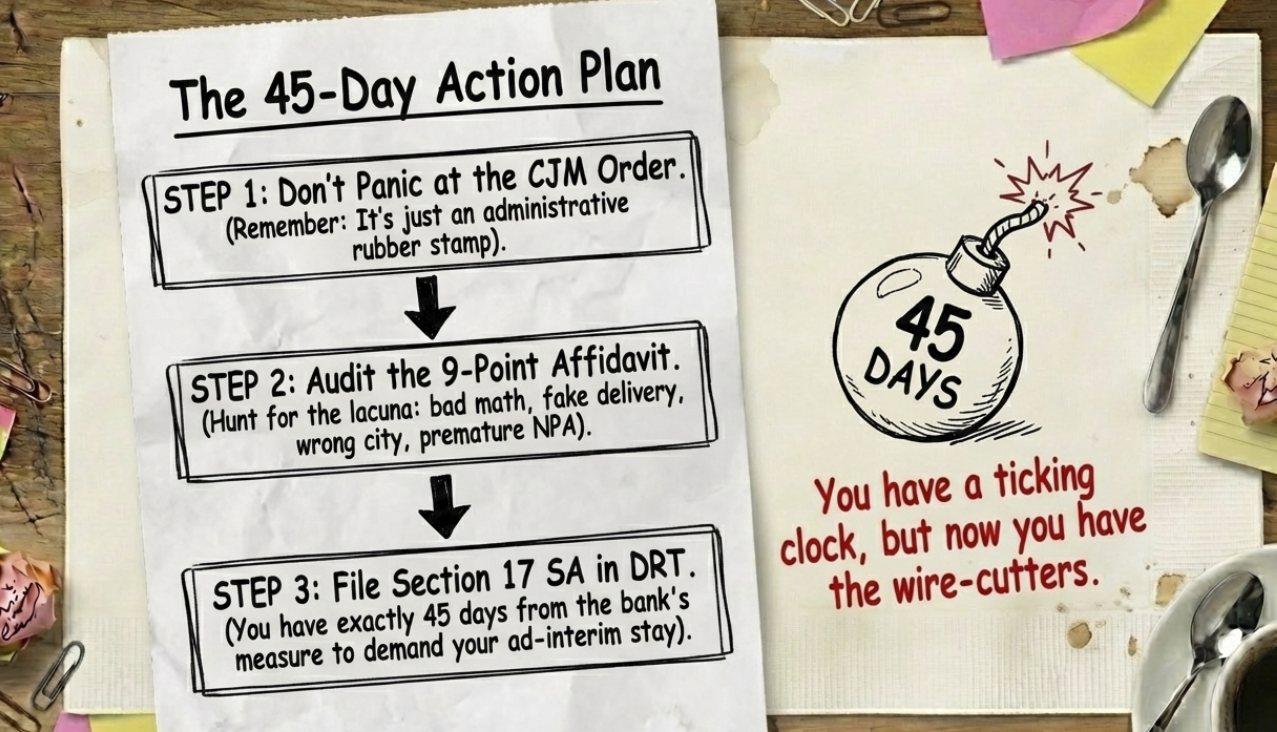

Many borrowers think a CJM order is the end of the road. It isn’t. The Magistrate’s role is administrative—they must verify a 9-point affidavit filed by the bank.6 If this affidavit contains errors, such as an incorrect NPA date or missing proof of notice service, the order is legally flawed.

Top Grounds for a DRT Stay:

- Illegal NPA Classification: Did the bank follow the 90-day default norm? If not, the entire process is void.9

- Agricultural Land: Banks cannot seize agricultural land under SARFAESI. This is a common “lacuna” that stops banks in their tracks.17

- Lack of Notice: If you didn’t receive the Section 13(2) notice or if the bank ignored your Section 13(3A) objections, you have a strong case for an immediate stay.11

How the Debt Recovery Tribunal (DRT) Protects You

You have 45 days to file a Securitisation Application (SA) in the DRT.2 Unlike appeals, filing in the DRT often does not require a heavy pre-deposit of the debt.28 The DRT can:

- Grant an interim stay to prevent the bank from taking your keys.

- Stop a property auction even if a sale date is set.10

- Restore possession if the bank has already acted illegally.2

Expert DRT Leal Services

Navigating SARFAESI litigation requires more than just knowing the law; it requires identifying the specific procedural gaps the bank left behind. Our DRT legal specialists excel at:

- Auditing bank affidavits for Section 14 lacunas.

- Filing urgent stay applications to protect residential and commercial property.

- Challenging wrongful NPA status.

- Securing One-Time Settlements (OTS) through tactical litigation.

Stop the auction today. If you have a Section 14 summons or a possession notice, contact our SARFAESI defense team for an immediate consultation.

Works cited

- Understanding Section 13(4) of SARFAESI Act | Bajaj Finance, accessed on March 27, 2026, https://www.bajajfinserv.in/understanding-sec-13-4-of-sarfaesi-act

- SARFAESI Act: Balancing Debt Recovery & Borrower Rights – Maheshwari & Co., accessed on March 27, 2026, https://www.maheshwariandco.com/blog/sarfaesi-act-balancing-debt-recovery-borrower-rights/

- What are differences between Section 13 and 14 of SARFAESI Act, 2002 and Can High Court in exercise of Article 226 interfere with Order passed by CJM under Section 14 of the SARFAESI Act, 2002? – M/s Ablum Electrical Industries Vs. Authorised Officer, Cluster Head, J&K Bank, Pulwama. – Jammu & Kashmir and Ladakh High Court – IBC Laws, accessed on March 27, 2026, https://ibclaw.in/m-s-ablum-electrical-industries-vs-authorised-officer-cluster-head-jk-bank-pulwama-jammu-kashmir-and-ladakh-high-court/

- Section 14 of the SARFAESI Act Explained: Procedure, Challenges, and Legal Remedies for Indian Lenders – Legodesk, accessed on March 27, 2026, https://legodesk.com/section-14-of-the-sarfaesi-act-explained-procedure-challenges-and-legal-remedies-for-indian-lenders/

- Section 14 of SARFAESI Act: Key Provisions, Amendments, Procedure & Case Laws, accessed on March 27, 2026, https://thelegalschool.in/blog/section-14-sarfaesi-act

- (1) Where the possession of any secured assets is required to be taken by the secured creditor or if any of the secured assets is required to be sold or transferred by the secured creditor under the provisions of this Act, the secured creditor may, for the purpose of taking possession or control of any such secured assets, request, in writing, the Chief Metropolitan Magistrate or the District Magistrate within whose jurisdiction any such secured asset or other documents relating thereto may be situated or found, to take possession thereof, and the Chief Metropolitan Magistrate or as the case may be, the District Magistrate shall, on such request being made to him – India Code: Section Details, accessed on March 27, 2026, https://www.indiacode.nic.in/show-data?actid=AC_CEN_2_11_00037_200254_1517807324604§ionId=20656§ionno=14&orderno=17

- ISSUE XI : Section 17 of SARFAESI: Is it effective for the borrowers?, accessed on March 27, 2026, https://psalegal.com/issue-xi-section-17-of-sarfesi-is-it-effective-for-the-borrowers/

- A Borrower Can Now Challenge Symbolic Possession Under The SARFAESI Act, accessed on March 27, 2026, https://www.khaitanco.com/thought-leadership/a-borrower-can-now-challenge-symbolic-possession-under-the-SARFAESI-act

- Order Sheet (Continuation) – DRT, accessed on March 27, 2026, https://cis.drt.gov.in/drtlive/order/pdf/pdf1.php?file=L3VwbG9hZHMvZHJ0L2RydGNvdXJ0L2RhaWx5X29yZGVyLzIwMjQvTWF5LzE5MDEzMDAwNTI0MjAyM18yZDM1NzFkNTY4ZjZhMjJjZjZmMGQxYTFmM2RjODg2OS5wZGYqKio1Nzc0NCMxI2tvbGthdGEz

- What to Do When a Bank Files a Case in DRT? Your Legal Options – The Law Brigade Publishers, accessed on March 27, 2026, https://thelawbrigade.com/general-research/what-to-do-when-a-bank-files-a-case-in-drt-your-legal-options/

- Deciding objection raised under Section 13(3A) of SARFAESI Act, 2002 is certainly not an empty formality, but all the grounds raised by Borrowers are required to be considered by Bank – Subhashree Ram Garments Pvt. Ltd. and Ors. v. The Authorized Officer, Union Bank of India and Ors. – Madras High Court – IBC Laws, accessed on March 27, 2026, https://ibclaw.in/subhashree-ram-garments-pvt-ltd-and-ors-v-the-authorized-officer-union-bank-of-india-and-ors-madras-high-court/

- Debtor’s Right to Hearing in SARFAESI Section 14? Explained – Supreme Today AI, accessed on March 27, 2026, https://supremetoday.ai/issue/debtor’s-right-to-hearing-in-sarfaesi-section-14

- Important Supreme Court and High Court Judgments of 2022 on SARAFESI Act, 2002/ Recovery of Debts and Bankruptcy Act, 1993 – IBC Laws, accessed on March 27, 2026, https://ibclaw.in/important-supreme-court-and-high-court-judgments-of-2022-on-sarafesi-act-2002-recovery-of-debts-and-bankruptcy-act-1993/

- Tenant Rights in SARFAESI Context | PDF | Law – Scribd, accessed on March 27, 2026, https://www.scribd.com/document/457328549/New-Microsoft-Word-Document-2

- Section 17 of SARFAESI Act, 2002: Right to Appeal, Provisions & Case Laws, accessed on March 27, 2026, https://thelegalschool.in/blog/section-17-sarfaesi-act

- SC Clarifies Civil Court Jurisdiction in Property Disputes Amid SARFAESI Proceedings, accessed on March 27, 2026, https://foxmandal.in/News/sc-clarifies-civil-court-jurisdiction-in-property-disputes-amid-sarfaesi-proceedings/

- Calcutta High Court upholds rejection of UCO Bank’s SARFAESI application by District Magistrate over Affidavit defects – SCC Online, accessed on March 27, 2026, https://www.scconline.com/blog/post/2025/06/25/calcutta-high-court-dm-upholds-uco-bank-sarfaesi-application-rejected-legal-news/

- IN THE HIGH COURT OF JUDICATURE OF BOMBAY BENCH AT AURANGABAD (Erstwhile Andhra Bank),, accessed on March 27, 2026, https://bombayhighcourt.nic.in/generatepdf.php?bhcpar=cGF0aD0uL3dyaXRlcmVhZGRhdGEvZGF0YS9hdXJqdWRnZW1lbnRzLzIwMjQvJmZuYW1lPTIzMDMwMDAxNjg1MjAyM18xMi5wZGYmc21mbGFnPU4mcmp1ZGRhdGU9JnVwbG9hZGR0PTEzLzEyLzIwMjQmc3Bhc3NwaHJhc2U9MTQxMjI0MTMyODU0Jm5jaXRhdGlvbj0yMDI0OkJIQy1BVUc6MjkzODUmc21jaXRhdGlvbj0mZGlnY2VydGZsZz1OJmludGVyZmFjZT1O

- WHEN BANK LOANS ARE NOT PROCEEDS OF CRIME: THE KARNATAKA HIGH COURT’S CLARIFICATION ON PMLA ATTACHMENTS. – Legal 500, accessed on March 27, 2026, https://www.legal500.com/developments/thought-leadership/when-bank-loans-are-not-proceeds-of-crime-the-karnataka-high-courts-clarification-on-pmla-attachments/

- Judgment reserved on 30.07.2025 Judgment delivered on 06.08.2025 HIGH COURT OF JUDICATURE AT ALLAHABAD (LUCKNOW) MATTERS UNDER A – Court Book, accessed on March 27, 2026, https://s3.courtbook.in/2025/08/protection-of-borrowers-under-the-sarfaesi-act-legal-provisions-clarified-by-courts.pdf

- M/S Tandon And Company Thru. Proprietor … vs Debt. Recovery Tribunal Lko. Thru. … on 16 January, 2026, accessed on March 27, 2026, https://indiankanoon.org/doc/12112641/

- Union Bank Of India vs M/S. Southern Cashew Exporters on 10 December, 2025, accessed on March 27, 2026, https://indiankanoon.org/doc/192751700/

- Supreme Court Reinforces Lessee Protections under the SARFAESI Act – CaseMine, accessed on March 27, 2026, https://www.casemine.com/commentary/in/supreme-court-reinforces-lessee-protections-under-the-sarfaesi-act/view

- INDIAN LAW REPORTS ALLAHABAD SERIES 15. Merely because a person lower in order of preference has encroached upon Gaon Sabha lan, accessed on March 27, 2026, https://www2.allahabadhighcourt.in/files_ilr/english/splitted/22391912022_19-04-2023_english.pdf

- Kerala High Court: Magistrate’s jurisdiction under Section 14 of SARFAESI Act cannot involve orders passed without application of mind – SCC Online, accessed on March 27, 2026, https://www.scconline.com/blog/post/2025/03/29/magistrates-jurisdiction-section-14-sarfaesi-act-kerala-hc/

- Bank Of Baroda Earlier Vijaya Bank Thru. … vs State Of U.P Thru. Prin. Secy. Deptt. Of … on 25 October, 2024 – Indian Kanoon, accessed on March 27, 2026, https://indiankanoon.org/doc/68979466/

- Judgments – Manupatra, accessed on March 27, 2026, https://updates.manupatra.com/roundup/tagsearch.aspx?tag=SARFAESI

- has to simply satisfy himself about the contents of the facts regarding nine points and should also record satisfaction in the order under Section 14 of the SARFAESI Act, 2002 – The Authorised Officer, AU Small Finance Bank Ltd. and Anr. Vs. Star International and Ors. – DRAT Kolkata – IBC Laws, accessed on March 27, 2026, https://ibclaw.in/the-authorised-officer-au-small-finance-bank-ltd-and-anr-vs-star-international-and-ors-drat-kolkata/