- Identify and challenge procedural defaults by the SARFAESI Act compliance to halt bank auctions.

- File before the DRT under Section 17; tribunal applies prima facie, irreparable loss, and balance of convenience test.

- Challenge defective demand notices, missing Section 13(3A) reasoned replies, or signatures by unauthorized officers as procedural lacunae.

- Attack possession and public notice defects: missing vernacular publication, improper affixture, or simultaneous notices that negate the 30-day sale period.

- Challenge valuation: unapproved or stale valuer reports and arbitrary reserve prices breaching Rule 8(5).

- Expect conditional stays requiring a pre-deposit of 25% to 50%; failure to deposit vacates the interim stay.

- Leverage the IBC moratorium for corporate borrowers; CIRP admission bars SARFAESI actions if sale certificate issued after insolvency commencement.

Comprehensive Legal Analysis of Procedural Remedies and Strategic Challenges to Bank Auctions under the SARFAESI Act

Creditor and contributor of this article:

Patra’s Law Chambers:

About Us:

Patra’s Law Chambers is a law firm with offices in Kolkata & Delhi, offering comprehensive legal services across various domains. Established in 2020 by Advocate Sudip Patra (Advocate, Supreme Court of India & Calcutta High Court) an alumnus of the Prestigious Rajiv Gandhi School of Intellectual Property Law, IIT Kharagpur ,with Post Graduate diploma in Business Law from IIM Calcutta, the firm specializes in Civil, Criminal, Writs,High Court Matters, Trademark, Copyright, Company, Tax, Banking, Property disputes, Service law, Family law, and Supreme Court matters.You can know more about us in here

Kolkata Office:

NICCO HOUSE, 6th Floor, 2, Hare Street, Kolkata-700001 (Near Calcutta High Court)

Delhi Office:

House no: 4455/5, First Floor, Ward No. XV, Gali Shahid

Bhagat Singh, Main Bazar Road, Paharganj, New Delhi-110055

Website: www.patraslawchambers.com

Email: [email protected]

Phone: +91 890 222 4444/ +91 7003 715 325

Click here to download the PDF of this particular blog.

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002, emerged as a legislative response to the systemic inefficiencies in the Indian debt recovery framework, particularly the protracted delays inherent in traditional civil litigation.1 Often colloquially referred to or searched as the “Surface Act” due to phonetic proximity, this statute provides secured creditors—primarily banks and financial institutions—with the extraordinary power to enforce security interests without the intervention of a court or tribunal.3 However, the exercise of this power is not absolute and is governed by a rigorous set of mandatory procedural rules. For a petitioner or borrower seeking to stop the auction of a court-attached property, the primary legal strategy involves identifying and challenging the “legal lacunae” or procedural defaults committed by the bank.5 These challenges are typically adjudicated by the Debt Recovery Tribunal (DRT) under Section 17, which acts as a vital judicial check on the potential for arbitrary enforcement.7

The Jurisprudential Landscape of Secured Interest Enforcement

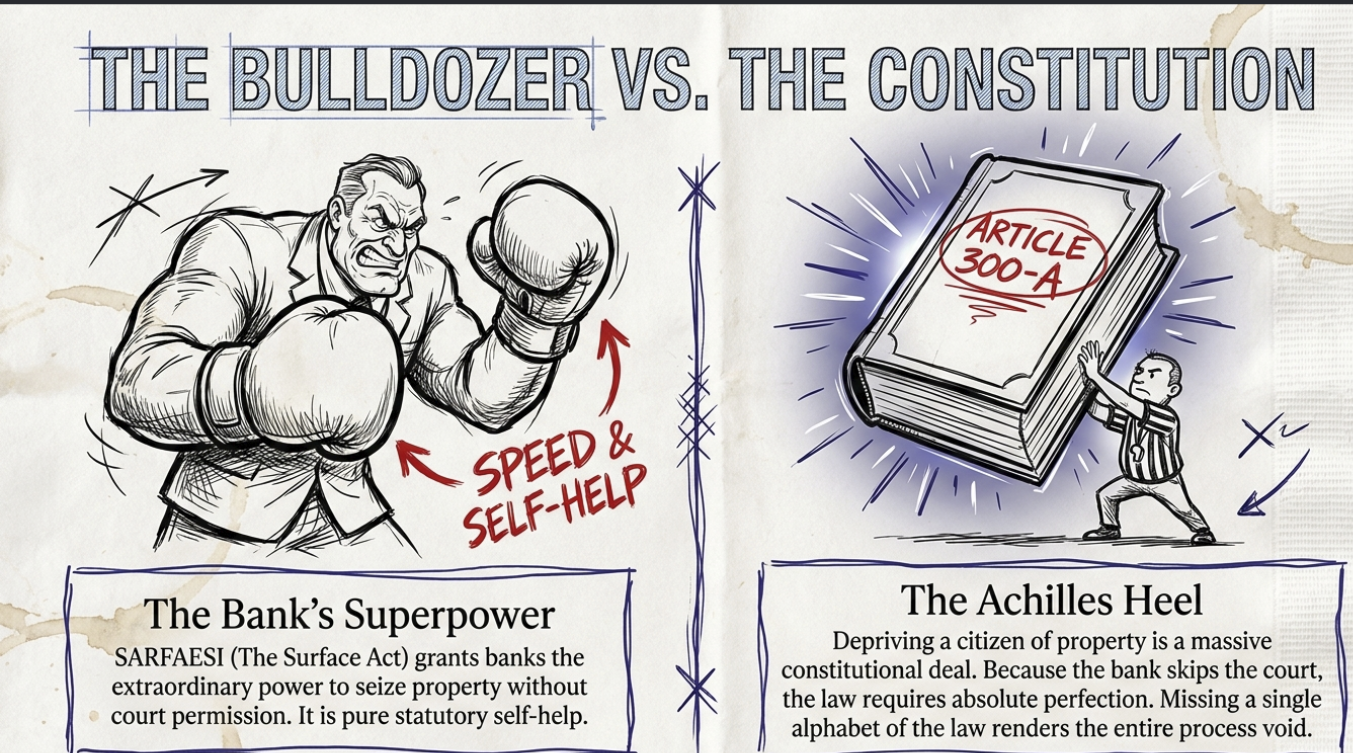

The SARFAESI Act operates on the principle of self-help for creditors, but its implementation is heavily scrutinized because it involves the deprivation of property, which remains a constitutional right under Article 300-A of the Constitution of India.9 The act is applicable only to secured loans that have been classified as Non-Performing Assets (NPAs) according to the stringent guidelines issued by the Reserve Bank of India (RBI).4 If a bank fails to strictly follow the “alphabet of the law” as laid out in the Security Interest (Enforcement) Rules, 2002, the entire recovery process—from the initial demand notice to the final issuance of a sale certificate—can be invalidated.9

Pre-requisites for Invoking SARFAESI Measures

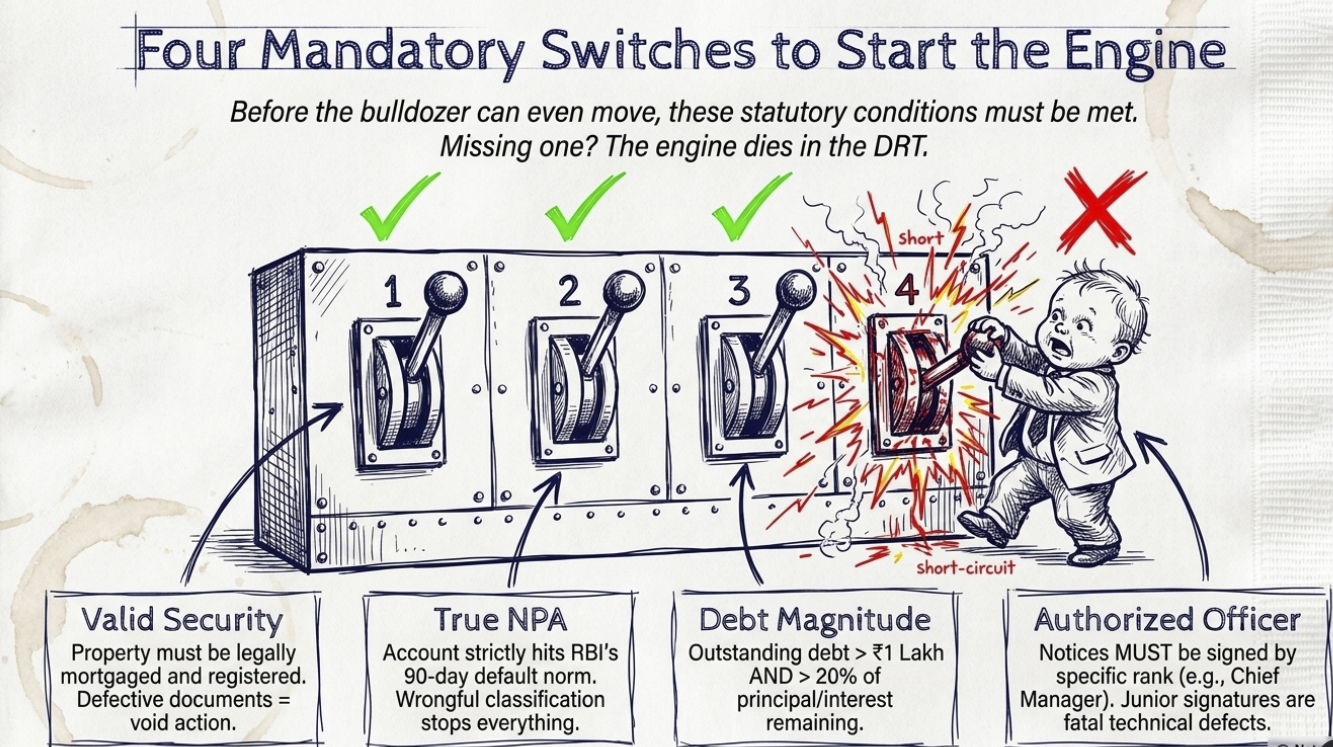

Before a bank can initiate an auction, several statutory conditions must be met. The absence of any of these conditions constitutes a fundamental legal lacuna that can be challenged in the DRT.6

| Statutory Requirement | Description and Legal Significance | Consequences of Non-Compliance |

| Valid Security Interest | The property must be legally mortgaged or hypothecated to the creditor. 4 | Action is void if the document is defective or unregistered. 8 |

| NPA Classification | The account must be classified as an NPA per RBI’s 90-day default norms. 4 | Wrongful classification stops all subsequent SARFAESI measures. 7 |

| Debt Magnitude | The outstanding debt must typically exceed one lakh rupees and be more than 20% of the principal/interest. | SARFAESI cannot be invoked for small or largely repaid debts. |

| Authorized Officer | Measures must be taken by an officer of a specific rank (e.g., Chief Manager in PSBs). 14 | Signature by an unauthorized or junior officer is a technical defect. 15 |

Strategic Identification of Legal Lacunae in the Demand Phase

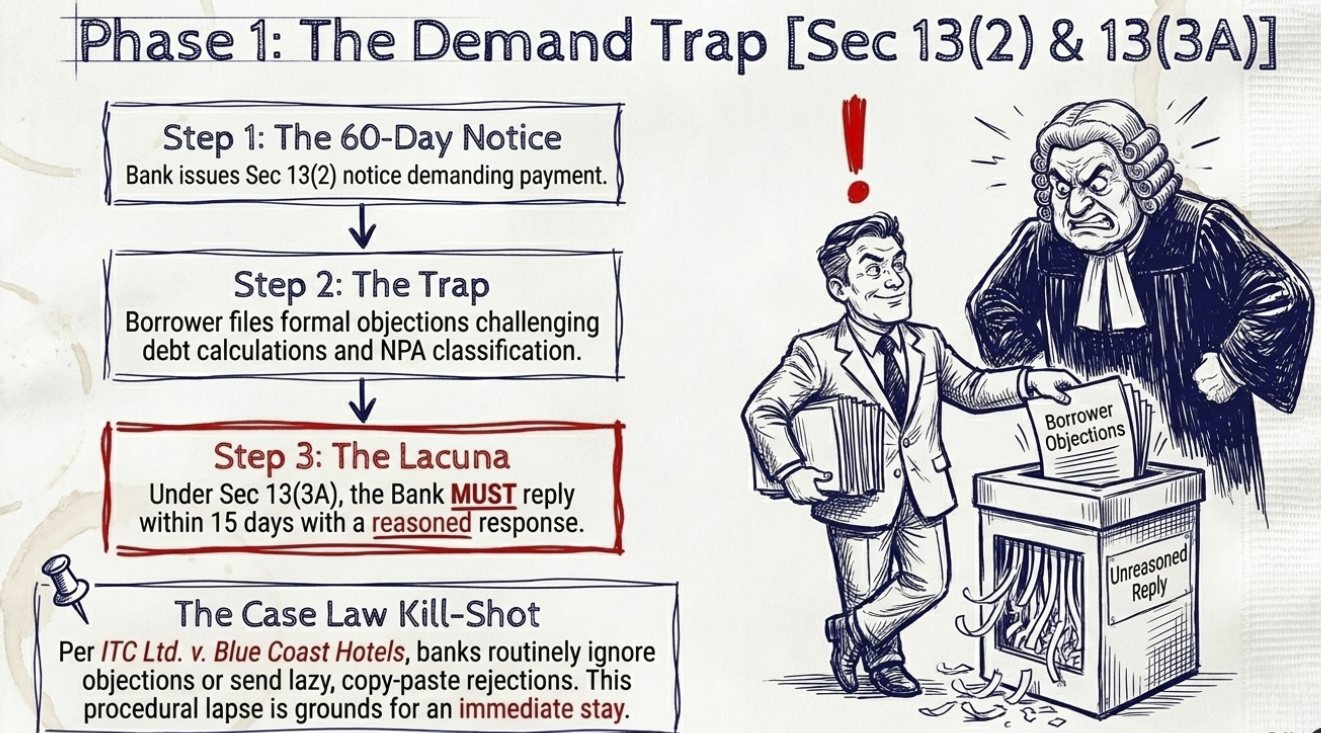

The enforcement process commences under Section 13(2) with a sixty-day demand notice.1 This phase is often where the first set of legal lacunae occurs. The notice must contain specific details of the debt and the security interest intended to be enforced.3

The Right to Object and the Reasoned Response

Following the landmark judgment in Mardia Chemicals Ltd. v. Union of India, Section 13(3A) was introduced to provide a semblance of natural justice.3 This section allows the borrower to raise objections within the sixty-day notice period.3 A critical lacuna arises if the bank fails to respond to these objections within fifteen days or provides a perfunctory, unreasoned rejection.3 In ITC Ltd. v. Blue Coast Hotels Ltd., the Supreme Court emphasized that the creditor’s response must be substantive; failure to communicate a reasoned reply is a procedural lapse that can be used to seek a stay on the auction.3

Challenging the Possession and Valuation Process

If the borrower fails to discharge the liability within sixty days, the bank proceeds to take possession under Section 13(4).1 This can be “symbolic possession,” achieved by serving and affixing a notice, or “physical possession,” often involving the assistance of a Magistrate under Section 14.17

Technical Defaults in Possession Notices

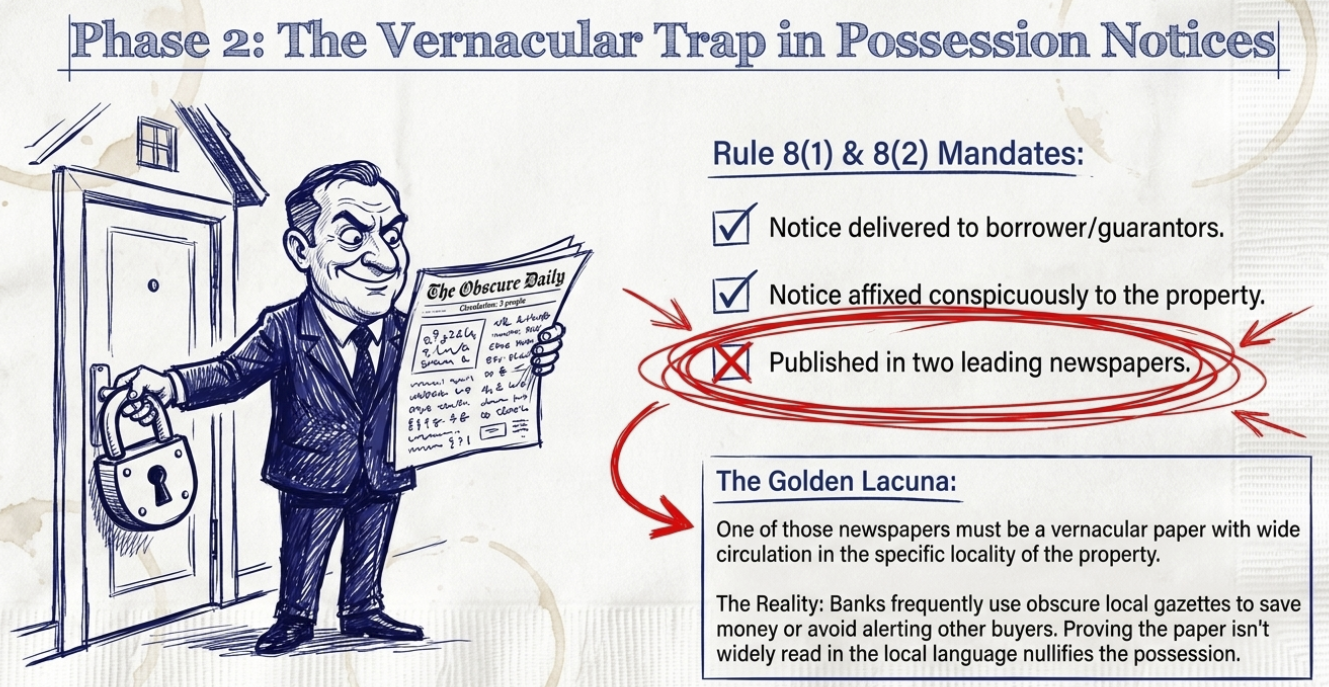

Rule 8(1) and 8(2) of the Security Interest Rules require the possession notice to be:

- Delivered to the borrower and guarantors.14

- Affixed to a conspicuous part of the property.6

- Published in two leading newspapers, one of which must be in a vernacular language.6

A frequent lacuna is the failure to publish in a newspaper that has “wide circulation” in the specific locality of the property.6 Petitioners often challenge auctions by proving the chosen newspaper is obscure or not widely read in the vernacular region, thereby failing the statutory requirement for public notice.6

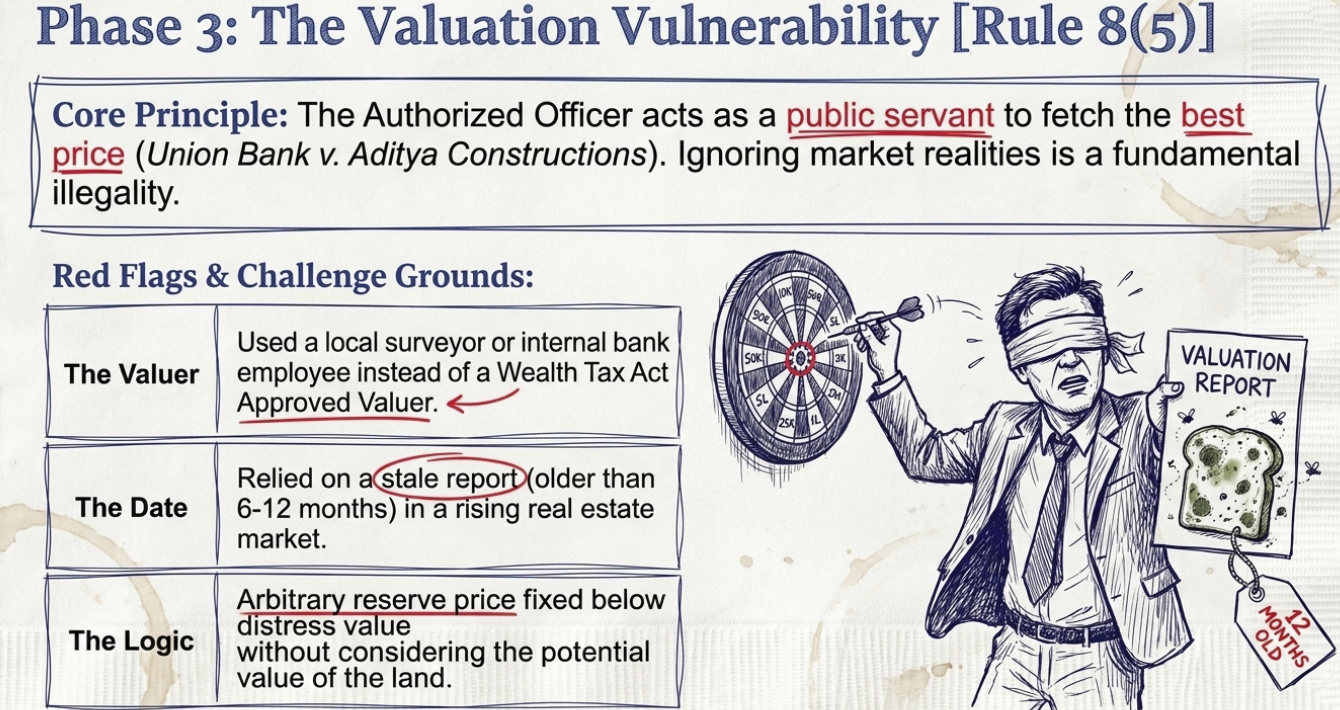

The Vulnerability of the Valuation Report

Rule 8(5) mandates that the authorized officer must obtain a valuation of the property from an approved valuer before fixing the reserve price.6 This is arguably the most contested area in DRT litigation.5

| Valuation Element | Mandatory Requirement | Common Lacuna for Challenge |

| Valuer Status | Must be an “approved valuer” (often under the Wealth Tax Act). 25 | Use of a local surveyor or an unapproved internal bank valuer. 25 |

| Reserve Price Fixation | Must be fixed “in consultation with the secured creditor.” 15 | Arbitrary fixation of reserve price below the “distress value” or fair market value. 23 |

| Recency of Report | The report must be contemporary to the sale. 28 | Use of a “stale” report (more than a year old) in a rising market. 26 |

| Disclosure of Logic | The report should show how the value was arrived at. 25 | Absence of reasoning or failure to consider the “potential value” of the land. 25 |

In Union Bank of India v. Aditya Constructions, the DRAT Kolkata noted that the authorized officer acts as a public servant and must ensure the property fetches the best possible price to reduce the borrower’s debt burden.15 A valuation that ignores market realities constitutes a “fundamental illegality”.12

Legal Grounds to Stop the Auction Sale Notice

The transition from possession to auction is governed by Rule 8(6) and Rule 9(1).14 These rules provide the borrower with a “last clear chance” to save the property.9

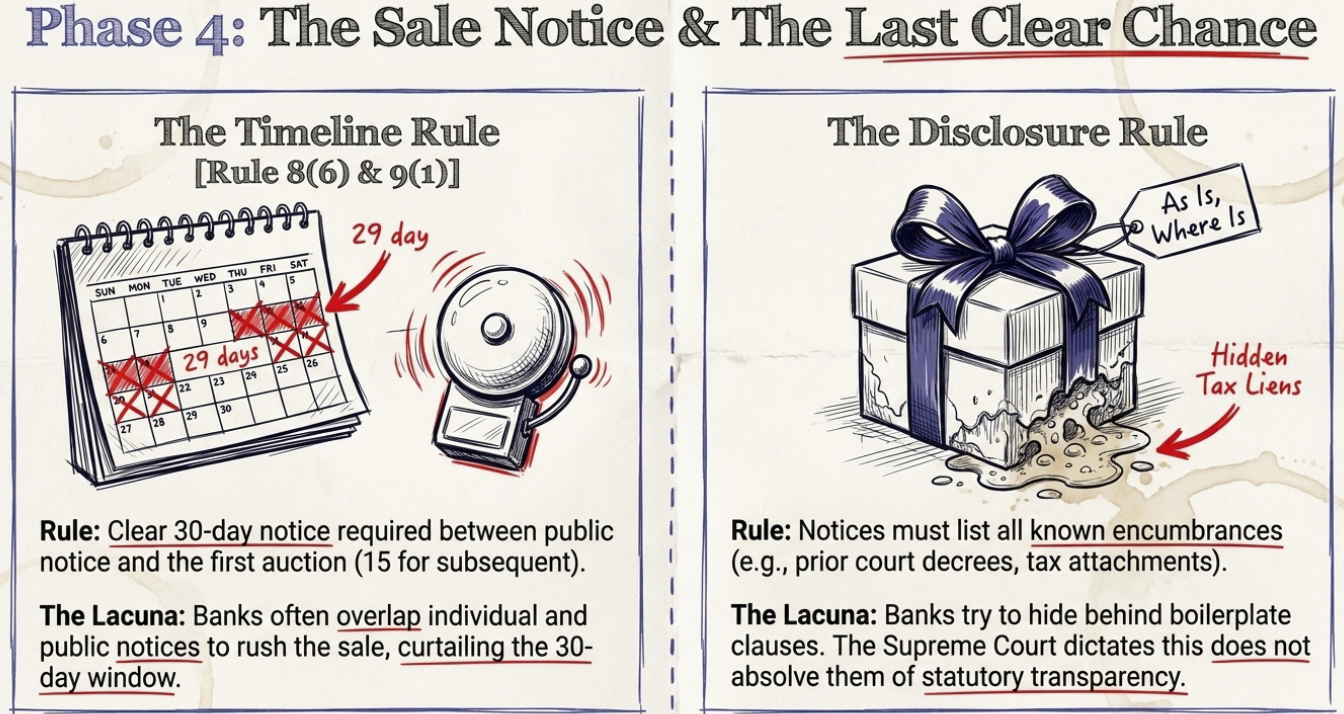

The Mandatory Thirty-Day Notice Period

For the first auction, the bank must provide a clear thirty-day notice to the borrower and the public.3 For subsequent auctions, if the first fails, this period may be reduced to fifteen days.26 A critical lacuna occurs if the bank issues the public notice (Rule 9(1)) simultaneously with the individual notice (Rule 8(6)) in a manner that curtails the borrower’s ability to redeem the property.30 While some courts allow simultaneous issuance, there must be a clear thirty-day gap between the publication and the date of sale.9

Defects in the Content of the Sale Notice

Under Rule 8(6), the sale notice must include:

- A detailed description of the immovable property.6

- Details of encumbrances known to the secured creditor.6

- The reserve price and the time/place of the auction.6

If a bank fails to disclose a known attachment by a tax authority or a prior court decree, it is a significant procedural lapse.6 Although banks often use “as is, where is” clauses, the Supreme Court has held that such clauses do not absolve the bank of its statutory duty to act fairly and transparently.19

Stay Orders and Remedies provided by the Debt Recovery Tribunal (DRT)

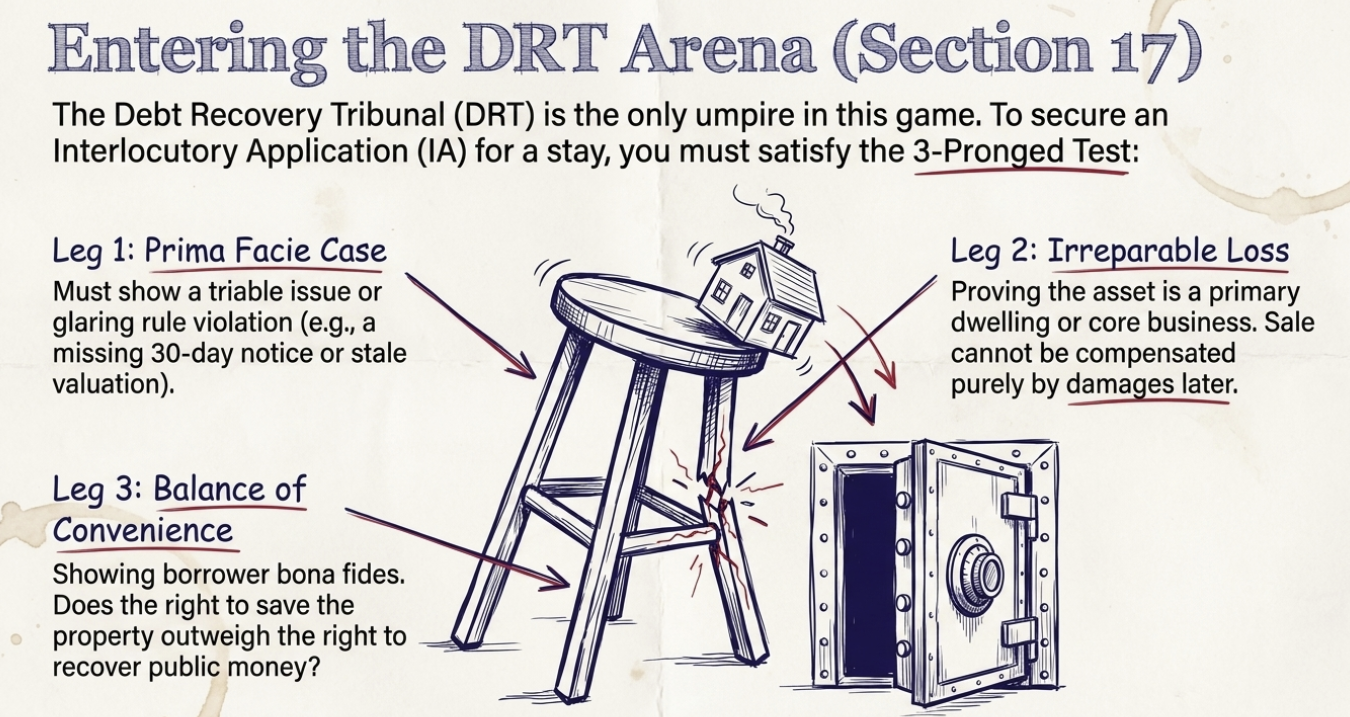

The Debt Recovery Tribunal (DRT) is the specific forum created to adjudicate SARFAESI disputes.2 Under Section 17, the DRT has the power to examine whether the measures taken by the bank are in accordance with the Act and Rules.7

Grounds for Granting a Stay Order

To stop an imminent auction, the petitioner files an interlocutory application (IA) for a stay.5 The DRT typically applies a three-pronged test:

- Prima Facie Case: The petitioner must show a “triable issue,” such as a clear violation of a mandatory rule (e.g., lack of vernacular publication or stale valuation).5

- Irreparable Loss: Since the property is often the borrower’s dwelling or primary business asset, its sale is considered an irreparable injury that cannot be compensated solely by damages.5

- Balance of Convenience: The tribunal weighs the bank’s interest in recovering public money against the borrower’s right to save their property. If the borrower is willing to show “bona fides” by depositing a portion of the dues, the balance usually tilts in favor of a stay.5

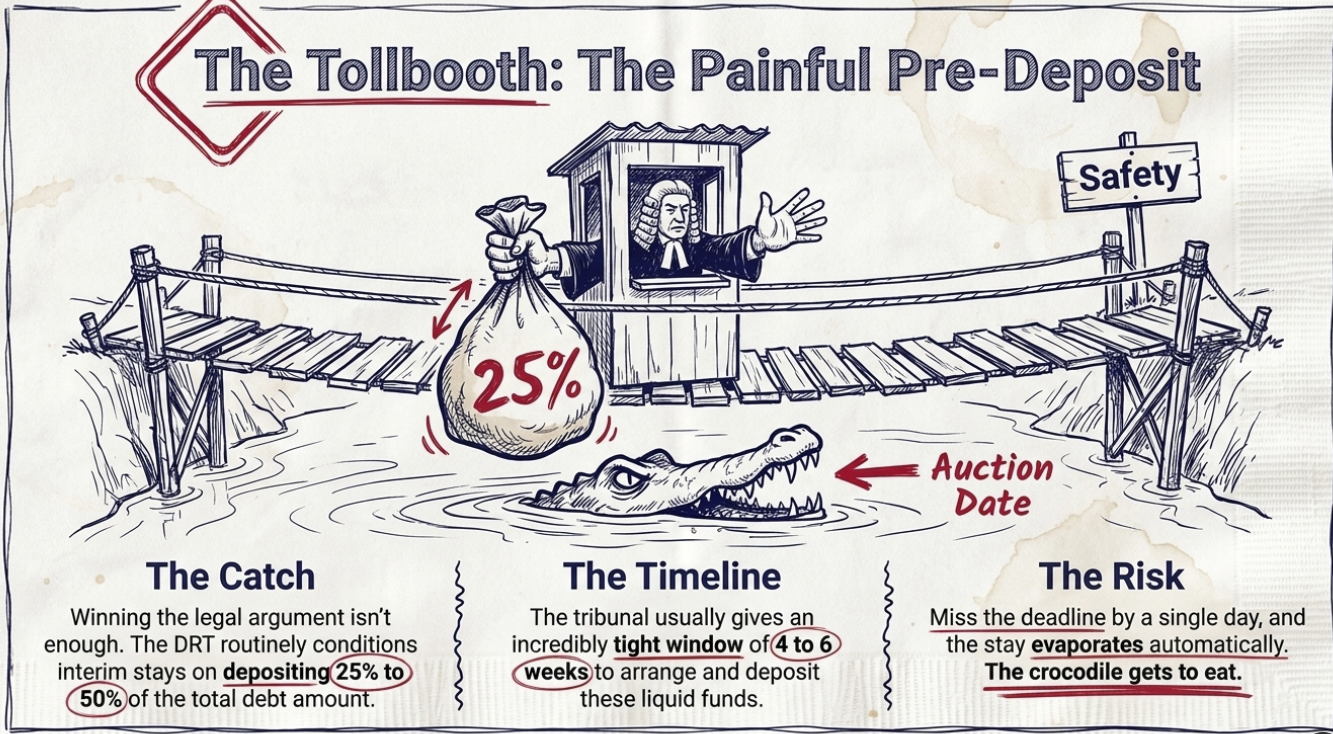

The Pre-Deposit Requirement and Conditional Stays

One of the primary hurdles for petitioners is the mandatory pre-deposit.7 While the DRT can grant an interim stay, it often conditions this stay on the deposit of 25% to 50% of the debt amount.7 If the borrower fails to make this deposit within the timeframe set by the DRT (e.g., four to six weeks), the stay order is vacated automatically, allowing the bank to proceed with the auction.29

Specific Orders the DRT Can Pass

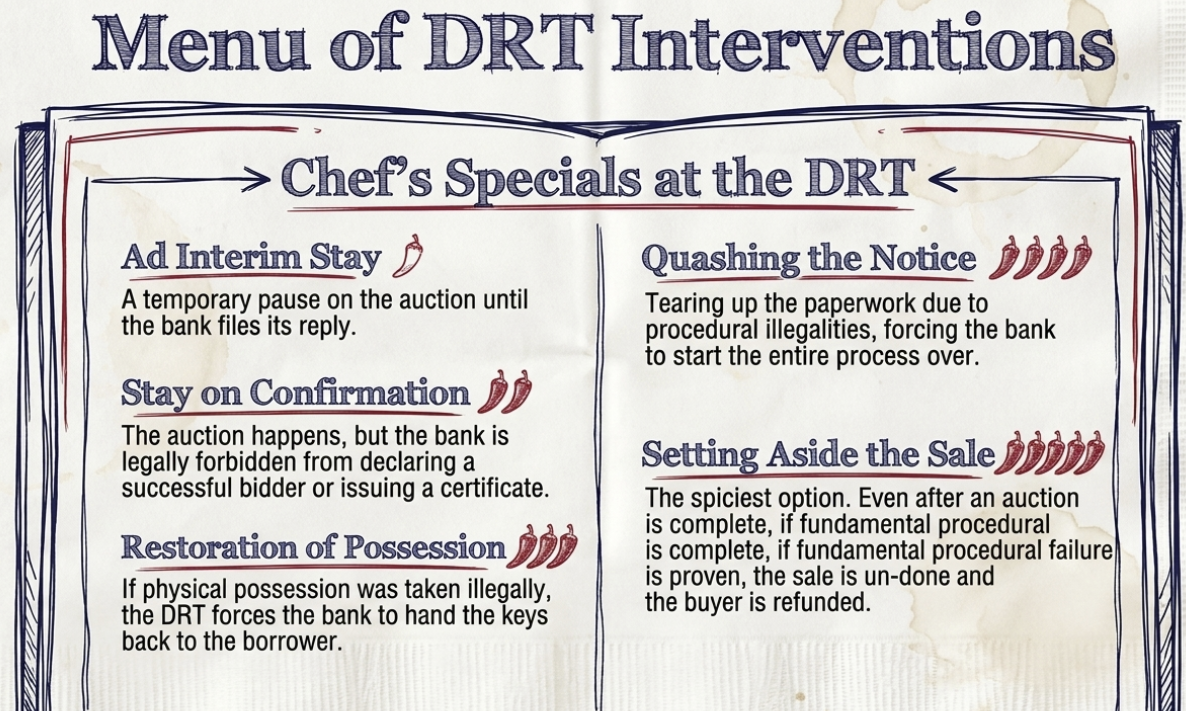

The DRT’s authority is comprehensive and includes the following:

- Ad Interim Stay: A temporary halt to the auction until the bank files its reply.5

- Stay on Confirmation of Sale: The auction may proceed, but the bank is forbidden from declaring a “successful bidder” or issuing a sale certificate.39

- Restoration of Possession: If the DRT finds the bank took physical possession illegally, it can order the property to be returned to the borrower.7

- Quashing the Sale Notice: Declaring the auction notice void due to procedural illegalities.23

- Setting Aside the Sale: Even after an auction is “complete,” if the petitioner can prove fraud or fundamental procedural failure (like a missing 30-day notice), the DRT can nullify the sale and order the return of the bid amount to the purchaser.23

Landmark Judgments Favoring the Petitioner

Understanding the “legal plough” (strategic roadmap) requires an analysis of the judicial precedents that have limited the bank’s powers.

The Right of Redemption Evolution

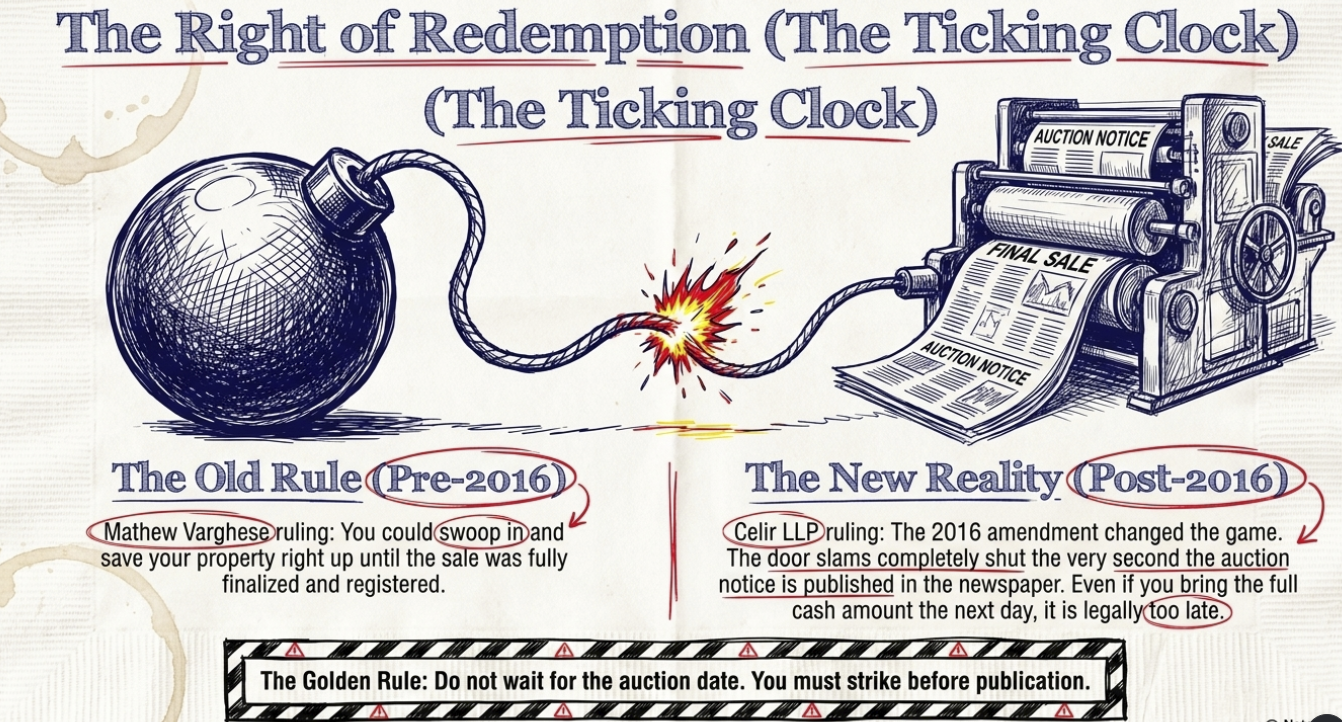

The “Right of Redemption” is the most potent weapon for a borrower.3

- Mathew Varghese v. M. Amritha Kumar (2014): The Supreme Court held that the mortgagor’s right to redeem the property is not lost even after possession is taken and survives until the sale is fully completed.10

- The 2016 Amendment Impact: Section 13(8) was amended to state that the right of redemption expires upon the “publication of the auction notice”.3

- Celir LLP v. Bafna Motors (2023) and M. Rajendran v. KPK Oils (2025): These recent rulings have strictly enforced the amended cutoff. The Supreme Court settled that post-2016, a borrower cannot redeem the property once the auction notice is published in the newspapers, even if they offer the full amount thereafter.3

Procedural Mandatory Nature

- Mardia Chemicals Ltd. v. Union of India (2004): This case is the bedrock of borrower rights, establishing that banks cannot act like “judge, jury, and executioner” and must provide a forum (DRT) for grievances before the property is sold.3

- Transcore v. Union of India (2008): While primarily assisting banks by allowing simultaneous remedies, it also clarified that SARFAESI measures must strictly follow the rules of the 2002 Enforcement Rules.3

- L&T Housing Finance Ltd. v. Trishul Developers (2020): This judgment added a nuance: “trivial” procedural lapses that do not cause “substantial prejudice” to the borrower may not be enough to stop an auction.12 Therefore, a petitioner’s challenge must focus on “fundamental” defects like missing notices or gross undervaluation.12

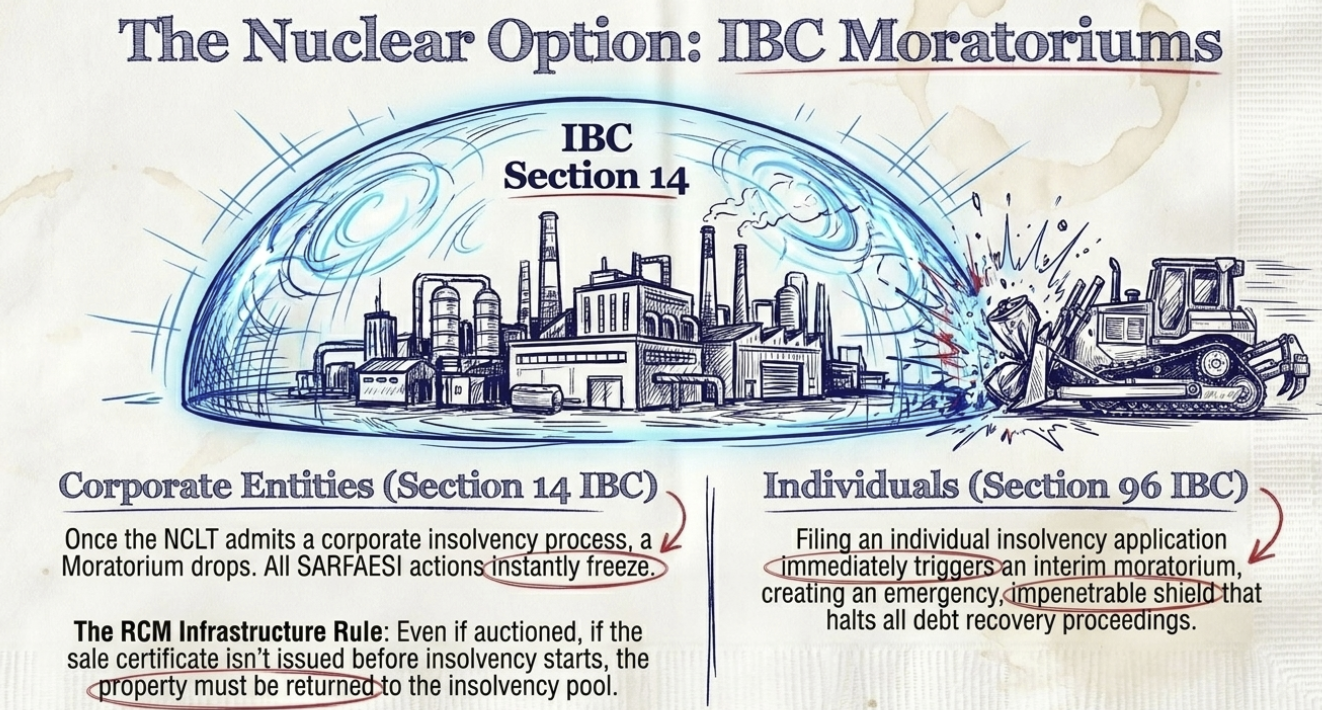

The IBC Moratorium: A Powerful Intervention

For properties attached to a corporate entity, the Insolvency and Bankruptcy Code (IBC), 2016, provides a “super-priority” mechanism to stop SARFAESI auctions.11

Under Section 14 of the IBC, once a Corporate Insolvency Resolution Process (CIRP) is admitted by the National Company Law Tribunal (NCLT), a “moratorium” is declared.43 This moratorium prohibits any action to recover or enforce any security interest.43 In Indian Overseas Bank v. RCM Infrastructure Ltd., the Supreme Court ruled that even if an auction is conducted, if the sale certificate is not issued before the insolvency commencement date, the sale becomes void and the property must be returned to the insolvency pool.43 For individual borrowers, the filing of an insolvency application under Section 96 triggers an “interim moratorium” that similarly halts all recovery proceedings related to the debt.44

Legal Services and Strategic Roadmap (The Legal Plough)

Navigating the “labyrinth” of DRT litigation requires expert legal services and a clear strategy.

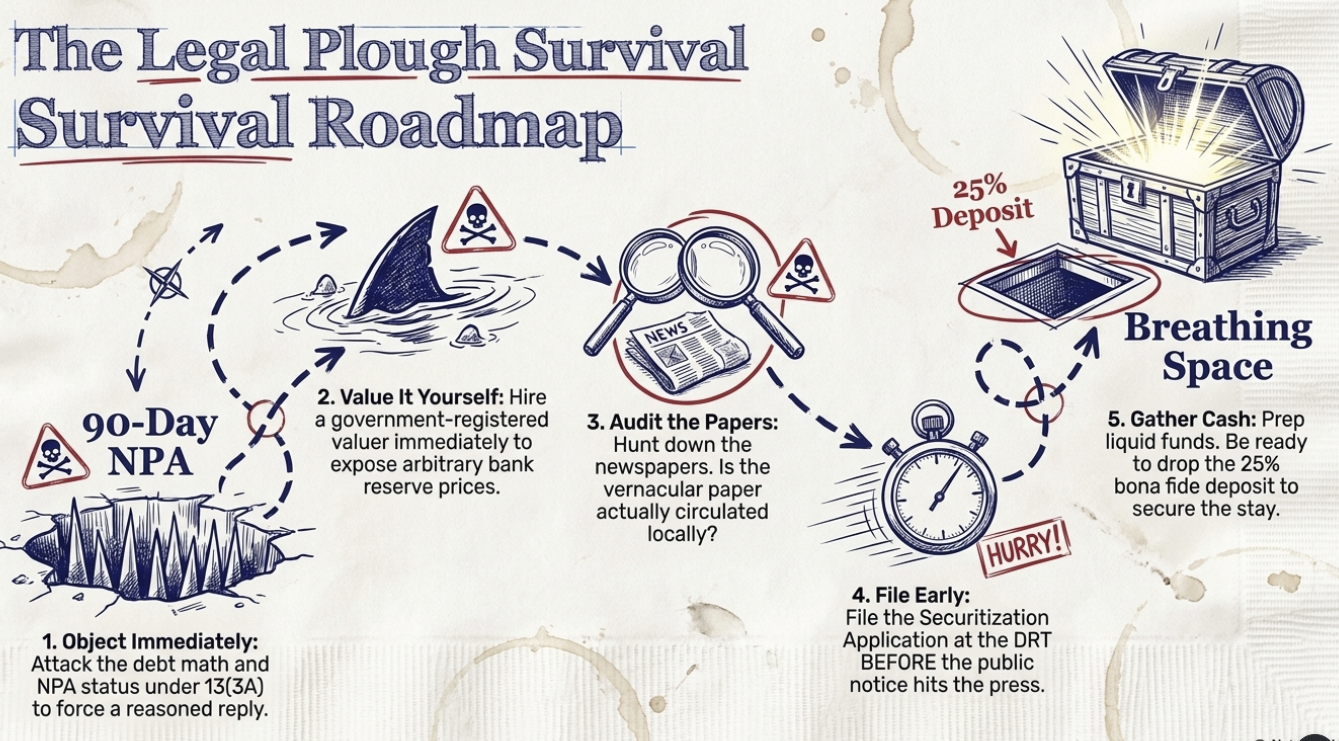

Practical Steps to Stop an Auction

- Immediate Objection: Upon receiving a 13(2) notice, file a detailed representation under 13(3A) challenging the debt calculation and the NPA status.3

- Independent Valuation: Obtain a valuation from a government-registered valuer to highlight discrepancies in the bank’s reserve price.25

- Search for Newspaper Defects: Verify if the newspaper chosen for the Rule 8(2) and Rule 9(1) notices is indeed widely circulated in the property’s locality.6

- File SA early: Do not wait for the auction date. Filing the Securitization Application immediately after the possession notice or sale notice increases the likelihood of getting a stay.5

- Bona Fide Deposit: Be prepared to deposit at least 25% of the claimed amount to secure a stay order.7

Directory of Specialized Legal Services

Professional intervention is often the difference between losing and saving a property. Several entities and individuals specialize in these “distressed asset” litigations:

| Service Provider / Expert | Specialty Area | Region / Focus |

| Justice League Lawyers | Specialist in SARFAESI and DRT appellate litigation. 2 | Chennai / South India |

| Ajay Gautam Advocate | Highly regarded for challenging wrongful enforcement and NPA advisement. 46 | Pan-India / Jabalpur / Delhi |

| Legals365 | Provides legal intervention to halt auctions and negotiate One-Time Settlements (OTS). 11 | Corporate and Residential Recovery |

| LRK & Associates | Consultancy for SARFAESI and debt restructuring. 48 | Mumbai / Thane |

| ASC Group | Comprehensive legal drafting for DRT applications and IBC filings. 45 | National / Corporate Restructuring |

Summary of Technical Defects to Challenge

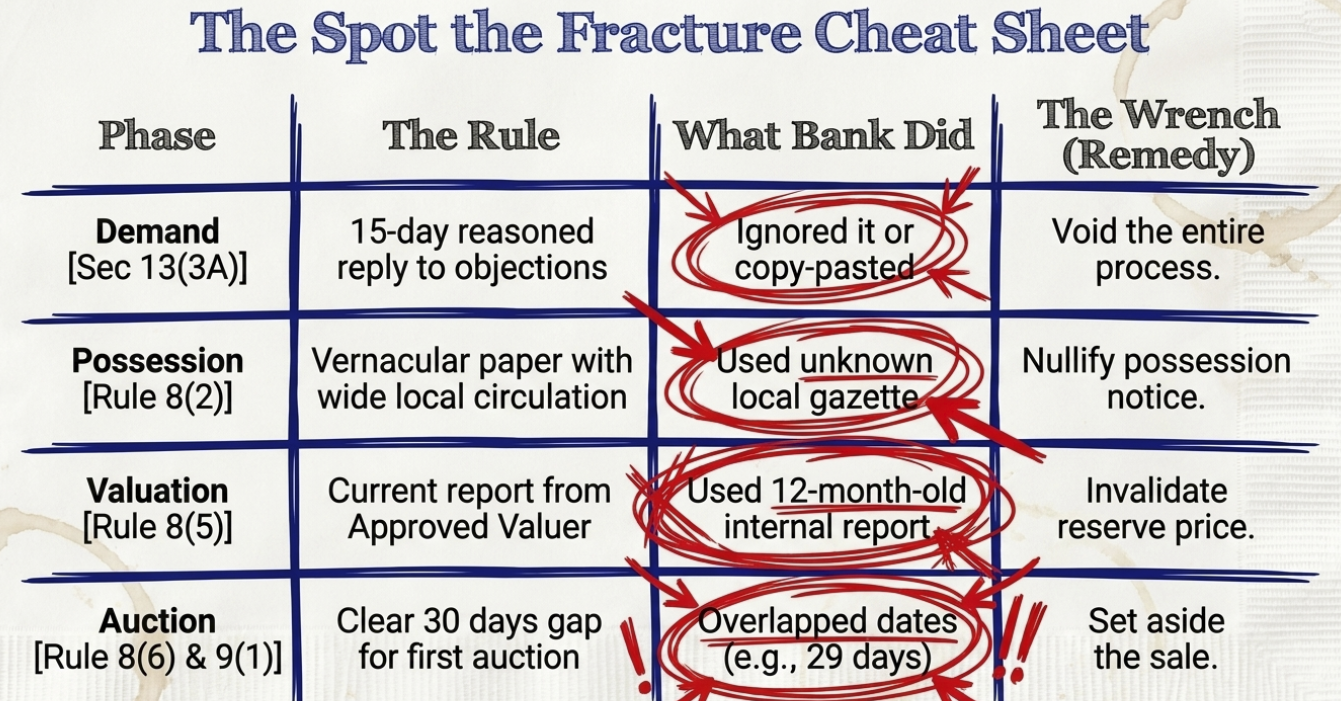

The following table summarizes the specific procedural lacunae that petitioners frequently use to successfully challenge and stop bank auctions in the DRT.6

| Phase of Recovery | Procedural Lacuna / Challenge Ground | Rule Violation |

| Demand Phase | Failure to provide a “reasoned response” to borrower objections within 15 days. 3 | Section 13(3A) |

| Possession Phase | Lack of publication in a “vernacular language” newspaper or missing affixture photographs. 6 | Rule 8(1) & 8(2) |

| Valuation Phase | Relying on a valuation report that is older than 6 to 12 months. 26 | Rule 8(5) |

| Auction Phase | Not providing a clear 30-day notice between publication and auction date. 9 | Rule 8(6) & 9(1) |

| Payment Phase | Extending the payment of the 75% balance beyond the statutory 90-day limit. 6 | Rule 9(4) |

| Administrative | The notice was signed by an officer who is not a “Chief Manager” or above (for PSBs). 14 | Rule 2(a) |

The complexity of the SARFAESI Act lies in its dual nature: it is a high-speed recovery tool for banks and a procedural minefield that requires absolute precision. For the borrower, the goal is not always to win the case on merits but to find the “procedural fracture” that halts the process, providing the necessary “breathing space” to negotiate a settlement or secure the funds to redeem the property before the finality of the auction notice publication.5 As judicial trends move toward protecting the “sanctity of the auction” for the sake of the banking economy, the petitioner’s window of opportunity is narrowing, making the early identification of legal lacunae more critical than ever before.26

Works cited

- Understanding Section 13(4) of SARFAESI Act | Bajaj Finance, accessed on March 27, 2026, https://www.bajajfinserv.in/understanding-sec-13-4-of-sarfaesi-act

- SARFAESI Act in Debt Recovery: Lawyers specializing in DRT and DRAT cases, accessed on March 27, 2026, https://www.drtlaw.in/2024/02/SARFAESI-Act-in-Debt-Recovery.html?m=1

- Section 13 of the SARFAESI Act: Enforcement of Security Interest – The Legal School, accessed on March 27, 2026, https://thelegalschool.in/blog/section-13-sarfaesi-act

- SARFAESI ACT, 2002- Applicability, Objectives, Process, Documentation – ClearTax, accessed on March 27, 2026, https://cleartax.in/s/sarfaesi-act-2002

- Stay on Bank Auction in Delhi – SARFAESI Act – Raizada Law Associates, accessed on March 27, 2026, https://www.raizadaassociates.com/blog/stay-on-bank-auction-in-delhi-sarfaesi-act/

- Procedure for Sale of Immovable Assets under SARFAESI Act 2002 …, accessed on March 27, 2026, https://ibclaw.in/procedure-for-sale-of-immovable-assets-under-sarfaesi-act-2002/

- Section 17 of SARFAESI Act, 2002: Right to Appeal, Provisions …, accessed on March 27, 2026, https://thelegalschool.in/blog/section-17-sarfaesi-act

- SARFAESI Act: Balancing Debt Recovery & Borrower Rights – Maheshwari & Co., accessed on March 27, 2026, https://www.maheshwariandco.com/blog/sarfaesi-act-balancing-debt-recovery-borrower-rights/

- SC: Statutory notice of sale of secured asset mandatory under SARFAESI, accessed on March 27, 2026, https://nishithdesai.com/default.aspx?id=4909

- Supreme Court Upholds SARFAESI Act Procedures in Mathew Varghese v. M. Amritha Kumar – CaseMine, accessed on March 27, 2026, https://www.casemine.com/commentary/in/supreme-court-upholds-sarfaesi-act-procedures-in-mathew-varghese-v.-m.-amritha-kumar/view

- How to Stop Bank Auctions on Home Loan Default? – Legals365, accessed on March 27, 2026, https://www.legals365.com/legal-advice/how-to-stop-bank-auctions-on-home-loan-default/

- Pahwa Buildtech (P) Ltd. v. Jagmohan Singh Arora | Delhi High Court | Judgment | Law, accessed on March 27, 2026, https://www.casemine.com/judgement/in/629a2a73b50db9bb596d95a4

- Security Interest: Meaning, forms, registration, enforcement, and effects of non-registration – Vinod Kothari Consultants, accessed on March 27, 2026, https://vinodkothari.com/wp-content/uploads/2023/05/Security-interest-meaning-forms-enforcement-etc.pdf

- Security Interest (Enforcement) Rules, 2002., accessed on March 27, 2026, https://www.arcindia.co.in/assets/img/Security-Interest-Enforcement-Rules-2002.pdf

- Authorised Officer is a public servant who has to perform his duties …, accessed on March 27, 2026, https://ibclaw.in/union-bank-of-india-vs-aditya-constructions-and-ors-drat-kolkata/

- 1.M/s.RKKR Steels Ltd Indian Bank; 2.Mr.Ritesh Raj ; 3.Mr.Rajiv Raj | Debts Recovery Tribunal | Judgment | Law | CaseMine, accessed on March 27, 2026, https://www.casemine.com/judgement/in/58d224a54a93261023a4f0a1

- The SARFAESI Act Step By Step Procedure For Asset Seizure – FinLender, accessed on March 27, 2026, https://finlender.com/the-sarfaesi-act-step-by-step-procedure-for-asset-seizure/

- Mardia Chemicals Ltd Litigation History – Supreme Today AI, accessed on March 27, 2026, https://supremetoday.ai/search/mardia-chemicals-ltd-litigation-history

- Buying an auctioned property? Here is everything you need to know – SNG & Partners, accessed on March 27, 2026, https://sngpartners.in/outside_perspective/buying-an-auctioned-property-here-is-everything-you-need-to-know/

- Security Interest (Enforcement) Rules, 2002 – LegitQuest, accessed on March 27, 2026, https://www.legitquest.com/act/security-interest-enforcement-rules-2002/9e6b

- Sale and auction under Sarfaesi Act – RKS Associate, accessed on March 27, 2026, https://www.rksassociate.com/sale-and-auction-under-sarfaesi-act/

- The Calcutta High Court has made a significant ruling regarding the SARFAESI Act, 2002. According to the judgment in VIJAY PRAKASH BOHRA VS STATE OF WEST BENGAL AND ORS (IA NO, accessed on March 27, 2026, https://lawchambersofpoojadua.com/the-calcutta-high-court-has-made-a-significant-ruling-regarding-the-sarfaesi-act-2002-according-to-the-judgment-in-vijay-prakash-bohra-vs-state-of-west-bengal-and-ors-ia-no-can-1-2025-a-secured/

- Challenge to auction sale under SARFAESI Act: DRAT KOLKATA – Dreamlaw, accessed on March 27, 2026, https://dreamlaw.in/challenge-to-auction-sale-under-sarfaesi-act-drat-kolkata/

- Non Reportable – DRT, accessed on March 27, 2026, https://cis.drt.gov.in/drtlive/order/pdf/pdf2.php?file=dXBsb2Fkcy9kcnQvZHJhdC9qdWRnZW1lbnQvMjAyNC9BcHJpbC8xOTEwOTAwMDIyNzIwMjJfOGY4NDY4YTI4NDJhNGE5Yjc2YmUwYjE1ZDE4MTkzZGUucGRmKioqMTIyNyMyI2tvbGthdGFkcmF0

- Rule 8(5) of Security Interest (Enforcement) Rules, 2002 only requires valuation to be obtained before effecting sale and does not prescribe a specific timeline | If Borrower is aggrieved by valuation made by the approved valuer of the Bank, he should have obtained another valuation report from some other approved valuer – Abhyidaya Farms Pvt. Ltd. Vs. Kanaka Mahalakshmi Agro Industries and Ors. – DRAT Kolkata – IBC Laws, accessed on March 27, 2026, https://ibclaw.in/abhyidaya-farms-pvt-ltd-vs-kanaka-mahalakshmi-agro-industries-and-ors-drat-kolkata/

- Completed Auction Can Be Set Aside Only for Fundamental Illegality – Fox Mandal, accessed on March 27, 2026, https://foxmandal.in/News/completed-auction-can-be-set-aside-only-for-fundamental-illegality/

- IDBI Bank Limited And Ors Vs. Sri Bijendra Kumar Singh And Ors On 14 March, 2023 – Legitquest, accessed on March 27, 2026, https://www.legitquest.com/case/idbi-bank-limited-and-ors-v-sri-bijendra-kumar-singh-and-ors/7739B2

- M/S.Mansarovar Pearls India Private … vs Canara Bank on 26 September, 2025, accessed on March 27, 2026, https://indiankanoon.org/doc/187631081/

- HIGH COURT FOR THE STATE OF TELANGANA ******** WRIT PETITION NOs.28320 AND 28947 OF 2018 WRIT PETITION No.28320 of 2018, accessed on March 27, 2026, https://csis.tshc.gov.in/hcorders/2018/wp/wp_28947_2018.pdf

- There is no need to wait for 30 days for publishing the sale notice under Rule 9(1) of the Security Interest (Enforcement) Rules, 2002 | Notices under Rule 8(6) and Rule 9(1) can be simultaneously issued after ensuring that there is clear 30 days gap between the publication of sale notice and the date of sale of the immovable secured asset – Bank of India Vs. Supreme Engineering Ltd. and Ors. – DRAT Mumbai – IBC Laws, accessed on March 27, 2026, https://ibclaw.in/bank-of-india-vs-supreme-engineering-ltd-and-ors-drat-mumbai/

- 1 REPORTABLE IN THE SUPREME COURT OF INDIA CIVIL APPELLATE JURISDICTION CIVIL APPEAL NO.1188/2025 (@Petition for Special Leave t, accessed on March 27, 2026, https://api.sci.gov.in/supremecourt/2019/37037/37037_2019_14_8_58808_Judgement_29-Jan-2025.pdf

- P&H High Court on SARFAESI Act and the Right of Redemption – IndiaCorpLaw, accessed on March 27, 2026, https://indiacorplaw.in/2022/01/14/ph-high-court-on-sarfaesi-act-and-the-right-of-redemption/

- Is It Safe to Buy Property Under the SARFAESI Act? A Comprehensive Legal Analysis, accessed on March 27, 2026, https://clawlaw.in/blog/Is%20It%20Safe%20to%20Buy%20Property%20Under%20the%20SARFAESI%20Act%3F%20A%20Comprehensive%20Legal%20Analysis

- SBI e-Auction Notice for Properties | PDF – Scribd, accessed on March 27, 2026, https://www.scribd.com/document/445450553/SBI-E-Auction-Document

- 25.04.2025 Judgment pronounced on – Delhi High Court, accessed on March 27, 2026, https://delhihighcourt.nic.in/app/showFileJudgment/68004062025CW139542018_144624.pdf

- M/S. Mahee Cotex vs Central Bank Of India, Authorised … on 25 July, 2022, accessed on March 27, 2026, https://indiankanoon.org/doc/105372710/

- Pre-deposit Under SARFAESI Act Must Be Made Before DRAT, Not Before Bank: Kerala HC [Read Judgment] – LawStreet Journal, accessed on March 27, 2026, https://lawstreet.co/judiciary/pre-deposit-under-sarfaesi-act-must-be-made-before-drat-not-before-bank-kerala-hc

- When properties are not shown to be divisible, it cannot be ascertained which specific part could be sold to satisfy the secured creditor’s claim under SARFAESI Act – Kotak Mahindra Bank Ltd. Vs. Venu Akula and Ors. – DRAT Kolkata – IBC Laws, accessed on March 27, 2026, https://ibclaw.in/kotak-mahindra-bank-ltd-vs-venu-akula-and-ors-drat-kolkata/

- K. Indra Mohan, vs Union Of India on 14 October, 2025 – Indian Kanoon, accessed on March 27, 2026, https://indiankanoon.org/doc/194639969/

- Right of Redemption and Foreclosure- Under SARFAESI Act – ELP …, accessed on March 27, 2026, https://elplaw.in/leadership/right-of-redemption-and-foreclosure-under-sarfaesi-act/

- Borrower’s Right of Redemption Extinguished on Publication of Auction Notice under SARFAESI – Supreme Court Observer, accessed on March 27, 2026, https://www.scobserver.in/supreme-court-observer-law-reports-scolr/sarfaesi-m-rajendran-v-kpk-oils-and-proteins-india-pvt-ltd/

- Between the Lines | Supreme Court: Trivial procedural lapses not a ground to nullify SARFAESI proceedings initiated by secured creditor if no substantial prejudice was caused to borrower, accessed on March 27, 2026, https://www.vaishlaw.com/supreme-court-trivial-procedural-lapses-not-a-ground-to-nullify-sarfaesi-proceedings-initiated-by-secured-creditor-if-no-substantial-prejudice-was-caused-to-borrower/

- Asset Reconstruction Companies In India: High-Handedness, Judicial Reckoning, And Regulatory Reform – Live Law, accessed on March 27, 2026, https://www.livelaw.in/articles/asset-reconstruction-companies-regulatory-reform-525230

- HC: IBC Moratorium to apply SARFAESI Sales unless Sale Certificate issued, Read Judgment – Latest Laws, accessed on March 27, 2026, https://www.latestlaws.com/case-analysis/hc-ibc-moratorium-to-apply-sarfaesi-sales-unless-sale-certificate-issued-read-judgment-232115/

- Legal Services in India – ASC Group, accessed on March 27, 2026, https://www.ascgroup.in/service/legal-services/

- Best DRT and Sarfaesi Lawyer in India Ajay Gautam Advocate, accessed on March 27, 2026, https://sites.google.com/site/drtdelhiadvocates

- Best DRT and Sarfaesi Lawyer in India Ajay Gautam Advocate – Google Sites, accessed on March 27, 2026, https://sites.google.com/site/drtjabalpuradvocates

- Top Sarfaesi Consultants in Mumbai – Best Securitisation And Reconstruction Of Financial Assets And Enforcement Of Security Interest Consultants near me – Justdial, accessed on March 27, 2026, https://www.justdial.com/Mumbai/Sarfaesi-Consultants/nct-11379419

- ISSUE XI : Section 17 of SARFAESI: Is it effective for the borrowers?, accessed on March 27, 2026, https://psalegal.com/issue-xi-section-17-of-sarfesi-is-it-effective-for-the-borrowers/